Proof of Income for a Personal Loan: Documents Lenders Accept

By ePaystubs Editorial Team | Updated June 22, 2026

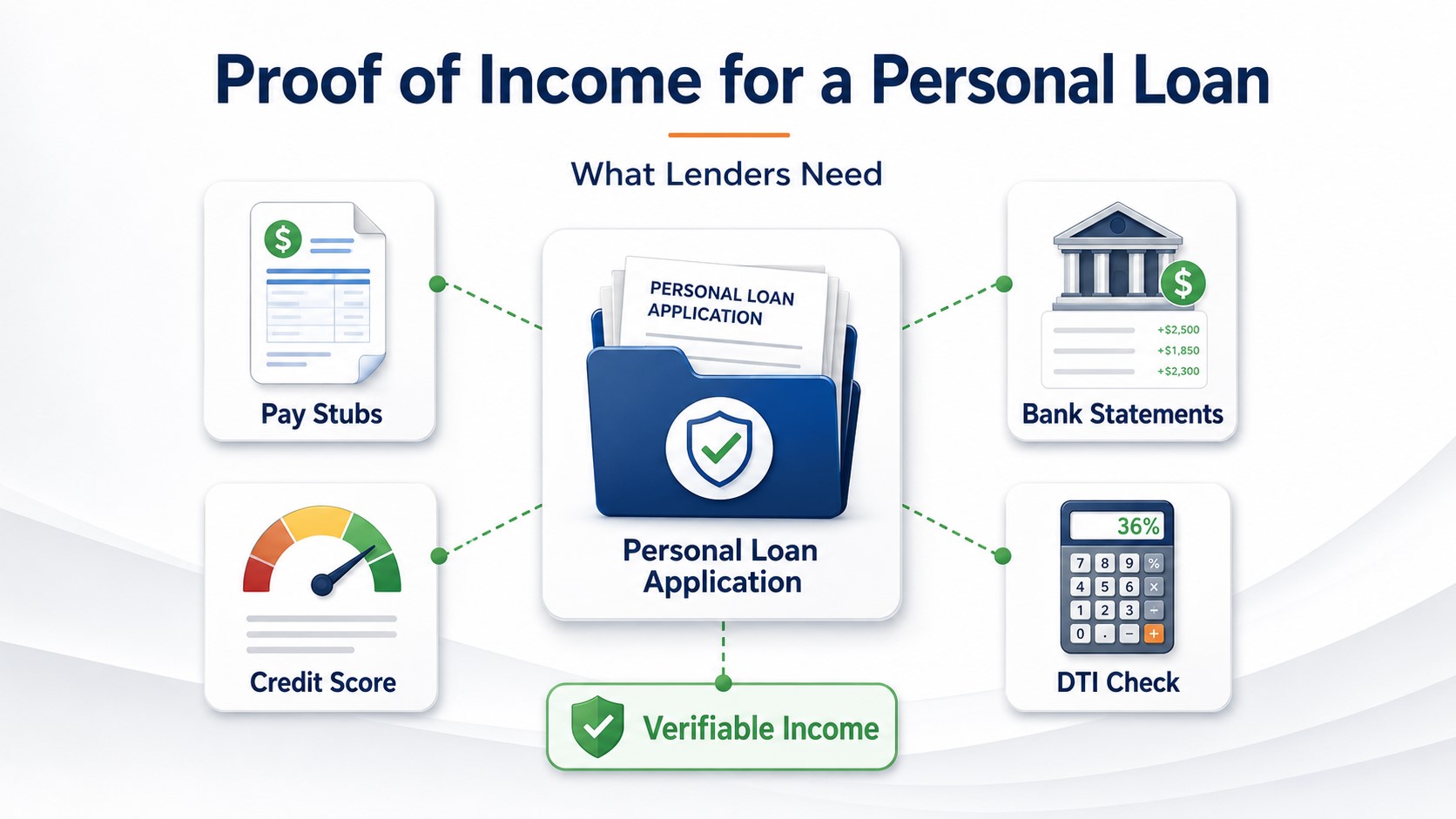

Most personal loans are unsecured, meaning there's no collateral backing them, so your income and credit are the lender's main protection, which makes proving your income matter more, not less. Lenders typically want proof of identity, income, address, and a bank account. For income, that's pay stubs, W-2s, tax returns, or bank statements. They weigh your income alongside your credit score and debt-to-income ratio. This guide covers the documents, what lenders evaluate, and how to prove your income cleanly.

A personal loan can cover almost anything, consolidating debt, a medical bill, a home repair, a wedding, and that flexibility is part of the appeal. But because most personal loans are not backed by anything you own, lenders look carefully at whether you can repay before they hand over the money. Proof of income is at the center of that decision. This guide walks through exactly which documents lenders want, how they weigh your income against your credit and your debts, and how to present your income cleanly so your application moves quickly. If you want to compare it against other borrowing, start with the general loan income requirements overview. One note up front: we are a pay-stub resource, not a lender, so treat this as a clear explainer of how personal-loan lenders think.

- Why income matters more

- Documents you'll need

- Credit, income, and DTI

- How much income

- How lenders verify

- Non-standard income

- Honesty and your pay stub

Why Income Matters More for an Unsecured Loan

Here is the distinction that shapes everything about a personal loan application. A car loan is backed by the car, and a mortgage is backed by the home, so if you stop paying, the lender can take the asset. Most personal loans are unsecured, there is no collateral the lender can seize.

One honest nuance: not every personal loan requires income proof. Some lenders approve based mainly on your credit score and your stated ability to repay. But it is common enough that you should be ready to back up whatever income you put on the application. A few lenders also offer secured personal loans, backed by a vehicle or your savings, which can have lighter income requirements but put your collateral at risk. This guide focuses on the standard unsecured kind. If you are looking at a car loan or a mortgage instead, those work differently, since both are secured by the thing you are buying.

The Documents You'll Need

Most lenders ask for documents in four categories, and you usually need just one document per category.

1 Proof of identity

A government photo ID, such as a driver's license, state ID card, or passport.

2 Proof of income

Pay stubs, W-2s, tax returns, or bank statements. This is the category we cover in depth below.

3 Proof of address

A utility bill, a lease, or an ID that shows your current address.

4 Bank account information

Required so the lender can deposit your funds. Most personal loans are funded by direct deposit.

For the income documents specifically, a traditional employee usually finds recent pay stubs easiest, while W-2s and tax returns give a fuller record. Bank statements work too, especially if your pay is direct-deposited, since the lender can look for consistent deposits.

What Lenders Evaluate: Credit, Income, and DTI

Income is not judged in isolation. Lenders weigh three things together, and how they balance out is what decides your approval.

Credit score

Your track record of repaying debt. No universal minimum; roughly 600 to 640 is a common floor, 670+ for better terms, 700+ for the best rates.

Income

Steady, verifiable, and enough for the loan. Stable income matters more than a high salary.

DTI

Your monthly debt payments divided by your gross monthly income. Lower is better.

How Much Income Do You Need?

The honest answer is that there is no universal minimum income for a personal loan. Lenders set their own, anywhere from under $20,000 to $100,000 or more, depending on the lender and the size of the loan.

On the debt side, most lenders prefer your total debt-to-income ratio to stay at or under about 36%, with some preferring 30% or less. DTI often determines your final approval and loan amount even when your credit score is strong, so it is worth calculating before you apply.

How Lenders Verify Your Income

The process follows a predictable structure, and knowing it helps you protect your credit score along the way.

- Prequalify. Most lenders let you prequalify with a soft credit check that shows estimated rates without hurting your score. No documents required yet.

- Apply and submit documents. You provide your income and identity documents.

- The lender validates. They verify and cross-check your information across sources for consistency, and may contact your employer directly.

- Underwriting decides. The lender finalizes your approval, your rate, and your loan amount.

If Your Income Is Non-Standard

Plenty of borrowers do not have a standard W-2 paycheck, and personal loans are still well within reach. Here is the short version, with deeper guides where the topic warrants one.

Benefits or retirement income counts too. Social Security, disability, and pension income are valid, just request a benefit verification letter to document them. No job or no traditional income is harder, but still possible with a cosigner (someone with stronger credit or income who shares legal responsibility for the loan) or a secured loan backed by collateral. A no-income-verification personal loan exists, but it generally requires exemplary credit.

A Note on Honesty (and Your Pay Stub)

Report your income accurately, and the reason is practical as much as ethical.

If you need a pay-stub-style document for your real income, you can create a pay stub in a few minutes and present it with your application.

Frequently Asked Questions

Not all, but most do. Some lenders approve based mainly on your credit score and stated ability to repay, but proof of income is common, so be ready to back up whatever income you list. Because personal loans are usually unsecured, lenders lean heavily on income to gauge repayment.

Pay stubs, W-2s, tax returns, and bank statements are the standard options. Self-employed borrowers typically use tax returns and bank statements. Benefit recipients can use a Social Security or disability verification letter. Many lenders also let you verify income by connecting your bank account online.

There's no universal minimum, but roughly 600 to 640 is a common floor, 670 or higher opens better terms, and 700+ gets the best rates. A lower score can still be approved if your income and debt-to-income ratio are strong, since lenders weigh all three together.

No universal minimum. Lenders set their own, ranging from under $20,000 to $100,000+ depending on the lender and loan size. Stable, verifiable income matters more than a high number, and the bigger the loan, the more income you'll need to show.

Most lenders prefer a debt-to-income ratio at or under about 36%, and some prefer 30% or less. DTI is your monthly debt payments divided by your gross monthly income. It often decides your final approval and loan amount even when your credit is strong.

Yes. You'll typically provide tax returns and bank statements instead of pay stubs, and possibly six to twelve months of records to show consistency. See our guide on proof of income when self-employed for the full documentation set.

It's possible but harder. Some lenders offer no-income-verification personal loans, but they usually require exemplary credit. Other routes are a cosigner with strong income or a secured loan backed by collateral. You'll still need to show some ability to repay.