Pre-Tax vs Post-Tax Deductions: How They Affect Your Paycheck and Taxes

By ePaystubs Editorial Team | Updated June 22, 2026 | Verified against IRS Publication 15-B

A pre-tax deduction comes out of your gross pay before taxes are calculated, which lowers your taxable income and increases your take-home pay. A post-tax deduction comes out after taxes are already withheld, so it does not reduce your tax bill. The same $100 deduction can cost you about $75 in take-home pay if it is pre-tax, but the full $100 if it is post-tax. Which is better depends on the benefit and your goals.

The order in which money leaves your paycheck decides how much tax you pay. Two employees earning the same salary can take home noticeably different amounts based only on whether their deductions come out before or after taxes. This guide explains the difference, walks through the exact payroll sequence, and covers the cases where a post-tax deduction is actually the smarter financial move.

- The core difference

- The payroll sequence

- Pre-tax and FICA

- Post-tax deductions

- When post-tax wins

- 2026 Roth catch-up rule

- Side-by-side

- Worked paycheck example

- On your W-2

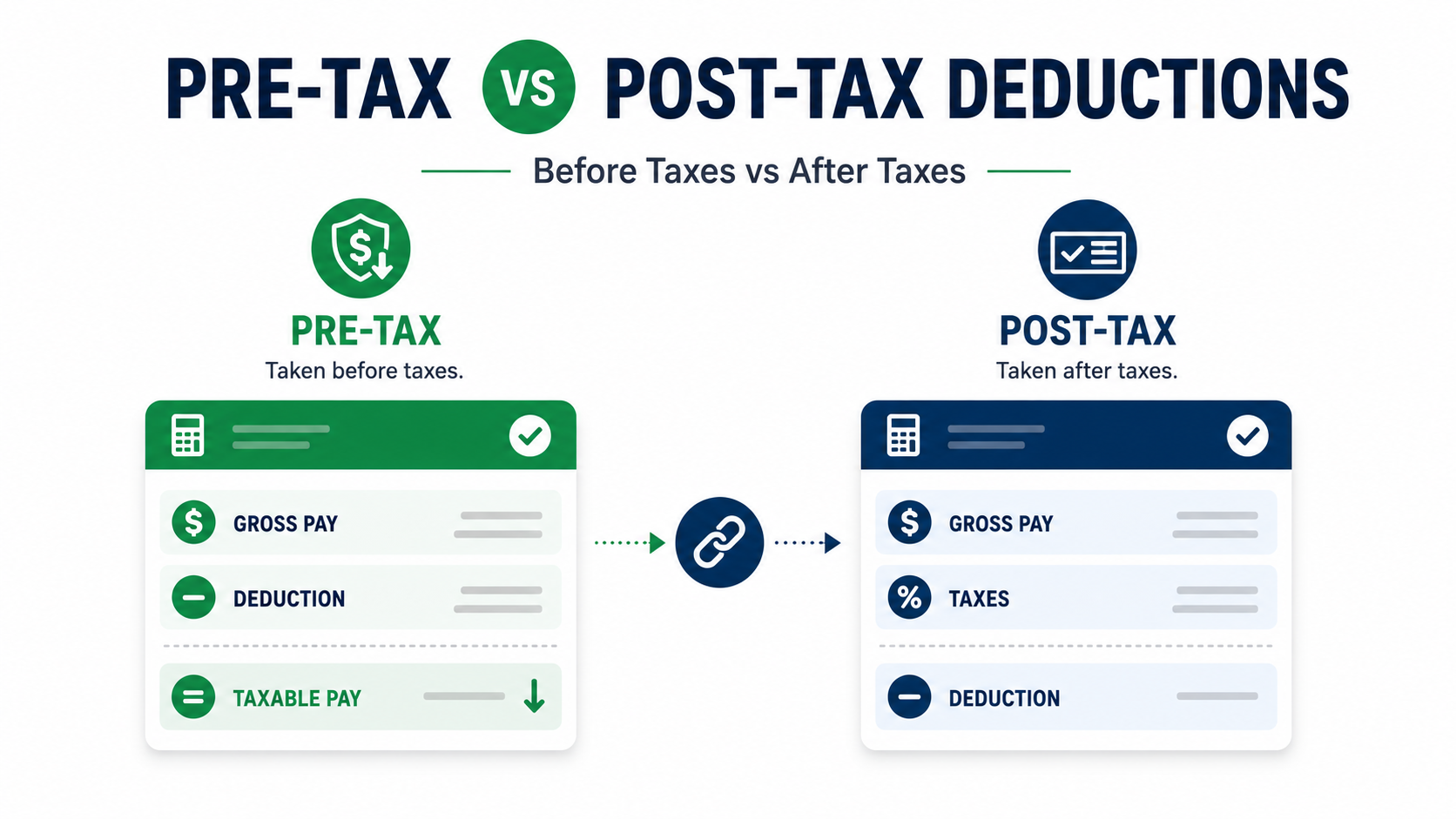

The Core Difference in One Sentence

A pre-tax deduction is subtracted from your gross pay before income and payroll taxes are calculated, so it shrinks the amount of income that gets taxed. A post-tax deduction is taken from pay that has already been taxed. The deduction itself never changes your gross pay. It only changes how much of that pay the government gets to tax.

That single distinction has a real dollar impact, and the clearest way to see it is to compare the same deduction handled both ways:

$100 Pre-Tax

$100 Post-Tax

The same pattern holds at any size. A $200 pre-tax deduction might lower your net pay by only $140 to $150, because you also stop paying tax on that $200. A $200 post-tax deduction removes the full $200 from your take-home pay. The tax savings on pre-tax deductions is exactly why they feel cheaper.

How the Two Affect Your Taxable Wages (The Payroll Sequence)

Every paycheck follows the same fixed order. Once you see where each deduction type sits in the sequence, the tax difference makes sense immediately.

The reason pre-tax deductions save you money is entirely about position. They come out at step 2, before the tax math in step 3, so they reduce the number your taxes are based on. Post-tax deductions come out at step 4, after the tax has already been calculated on the larger amount.

For exactly how this sequence shapes the wages that end up reported on your W-2, see your taxable wages.

Pre-Tax Deductions and the FICA Distinction

Here is the part most guides gloss over, and it is the single most important concept on your pay stub: not all pre-tax deductions reduce the same taxes. They split into two groups.

| Pre-Tax Deduction | Reduces Income Tax? | Reduces FICA? | 2026 Limit |

|---|---|---|---|

| Traditional 401(k) / 403(b) / 457 | Yes | No | $24,500 2026 |

| HSA (high-deductible plan required) | Yes | Yes | $4,400 individual / $8,750 family |

| Health FSA | Yes | Yes | $3,400 2026 |

| Dependent Care FSA | Yes | Yes | $7,500 raised by OBBBA |

| Health / dental / vision premiums (Section 125) | Yes | Yes | No IRS cap |

| Commuter / transit / parking | Yes | Yes | $340/month each |

For the full mechanics of why a traditional 401(k) still gets hit with Social Security and Medicare tax even though it lowers your income tax, see what FICA means on a pay stub. For contribution limits, employer matching, and catch-up rules in detail, see what 401k means on a pay stub.

Post-Tax Deductions and What They Cover

Post-tax deductions come out after every tax has been calculated and withheld. They do not reduce your current taxable income, but several of them deliver tax-free benefits down the road.

| Post-Tax Deduction | What It Is | Future Benefit |

|---|---|---|

| Roth 401(k) | Retirement contribution made with after-tax dollars | Qualified withdrawals are tax-free in retirement |

| Disability insurance (when funded post-tax) | Short-term or long-term disability premiums | Benefits received are tax-free |

| Union dues | Membership dues per a collective bargaining agreement | No federal deduction since the 2017 tax law |

| Voluntary / supplemental life insurance | Coverage you elect beyond employer-provided basic life | Keeps benefits from becoming taxable |

| Charitable payroll giving | Donations routed through payroll | Deductible if you itemize |

| Wage garnishments | Court-ordered child support, tax levies, defaulted loans | Involuntary, no tax benefit |

Union dues are always post-tax because the IRS does not allow pre-tax treatment for them. Garnishments are involuntary post-tax deductions. For how each of these appears on your stub and what the codes mean, see pay stub deduction codes.

When Post-Tax Is Actually the Smarter Choice

The common advice is that pre-tax is always better because it lowers your taxes. That is true for most everyday benefits, but it is not the whole story. For two specific deductions, paying tax now is often the smarter long-term move.

The underlying principle mirrors the classic Roth-versus-traditional retirement debate: do you want a tax break now, or a tax-free benefit later? The mathematically optimal answer depends on your future tax rate compared to today's. But the math is not the only factor, because some benefits arrive exactly when your income has dropped.

Disability Insurance: The Textbook Case

This is the clearest example of post-tax winning. The choice changes whether your future benefits are taxed:

Pre-Tax Premiums

Post-Tax Premiums

Why post-tax usually wins here: disability insurance typically replaces only about 60% of your salary. If those reduced benefits are then taxed, the gap between your old income and your disability income widens at the worst possible time. Receiving the benefit tax-free removes that uncertainty. Many financial advisors lean toward post-tax disability premiums even when the math is close, because taxes are far easier to pay while you are still working than during a period when you cannot.

Roth 401(k): The Retirement Case

A Roth 401(k) is funded post-tax, and qualified withdrawals in retirement are completely tax-free, including the investment growth. It tends to win for people who expect to be in a higher tax bracket later than they are now. A common strategy is to split contributions between a traditional and a Roth 401(k) to diversify your tax exposure, so some retirement income is taxed and some is not. Just remember the combined total cannot exceed the annual IRS limit. For the full Roth-versus-traditional breakdown, see what 401k means on a pay stub.

The 2026 Rule That Forces Some Catch-Ups to Be Post-Tax

A significant change took effect this year that removes the pre-tax option for certain high earners. If you are 50 or older and earned more than $150,000 in Social Security wages last year, you no longer get to choose.

In plain terms: a high earner who expected to make an extra pre-tax catch-up contribution to lower this year's taxable income is now legally required to make that contribution post-tax instead. The catch-up still happens, but it no longer reduces current taxable wages. For how catch-up contributions and the 2026 limits work in full, see what 401k means on a pay stub.

Pre-Tax vs Post-Tax: Side by Side

| Feature | Pre-Tax Deduction | Post-Tax Deduction |

|---|---|---|

| When it is taken | Before taxes are calculated | After taxes are withheld |

| Reduces income tax now? | Yes | No |

| Reduces FICA? | Section 125 yes, 401(k) no | No |

| Reduces take-home by | Less than the deduction amount | The full deduction amount |

| Future benefit tax treatment | Usually taxed when used or withdrawn | Often tax-free when used or withdrawn |

| Common examples | Health, HSA, FSA, traditional 401(k), commuter | Roth 401(k), disability, union dues, garnishments |

The practical rule of thumb: choose pre-tax for benefits you need right now and for immediate tax relief, such as health insurance, dependent care, and commuter costs. Lean post-tax when a tax-free future benefit matters more than today's savings, as with disability insurance and Roth retirement contributions.

A Worked Example: The Same $300, Three Different Outcomes

Tables explain the rules, but real numbers make the difference click. Here is one employee earning $70,000 a year, paid biweekly, who routes $300 per paycheck into a benefit. The only thing that changes across the three columns is the type of deduction. Watch what happens to take-home pay.

| Per Paycheck | $300 Pre-Tax (traditional 401k) |

$300 Post-Tax (Roth 401k) |

$300 Section 125 (health premium) |

|---|---|---|---|

| Gross pay | $2,692.31 | $2,692.31 | $2,692.31 |

| The $300 deduction | -$300.00 | -$300.00 | -$300.00 |

| Wages taxed for income tax | $2,392.31 | $2,692.31 | $2,392.31 |

| Wages taxed for FICA | $2,692.31 | $2,692.31 | $2,392.31 |

| FICA withheld (7.65%) | -$205.96 | -$205.96 | -$183.01 |

| Federal income tax (approx) | -$287.08 | -$323.08 | -$287.08 |

| Net pay | $1,899.27 | $1,863.27 | $1,922.22 most take-home |

All three employees put the same $300 toward a benefit, yet their take-home pay differs by up to $59 per paycheck. The pre-tax 401(k) leaves $36 more in the worker's pocket than the post-tax Roth, because the $300 escaped income tax. The Section 125 health premium does best of all, leaving nearly $23 more than the traditional 401(k) on top of that, because it escaped both income tax and FICA. That extra FICA saving is the dollars-and-cents proof of the distinction covered earlier.

How This Shows Up on Your Pay Stub and W-2

The pre-tax and post-tax split is the reason the gross pay on your final stub does not match Box 1 on your W-2. Pre-tax deductions reduce the taxable wages reported on your W-2; post-tax deductions do not.

Specifically, pre-tax items reduce W-2 Box 1 (federal taxable wages). Section 125 items also reduce Box 3 (Social Security wages) and Box 5 (Medicare wages). A traditional 401(k) reduces Box 1 but not Boxes 3 and 5, which is why those two boxes are often higher than Box 1. Post-tax deductions are included in your gross earnings but never reduce any of these taxable-wage boxes.

If your stub gross and W-2 Box 1 do not match, this is almost always why, and both numbers are correct. For the full box-by-box reconciliation, see pay stub deduction codes and your taxable wages. When you need a record that itemizes pre-tax and post-tax lines correctly, you can generate a pay stub that lays them out clearly.

Frequently Asked Questions

For most everyday benefits like health insurance, dependent care, and commuter costs, pre-tax is better because it lowers your taxable income and increases take-home pay. But post-tax can be the smarter choice for disability insurance and Roth retirement contributions, where paying tax now means the future benefit arrives tax-free.

Some do, some do not. Section 125 benefits such as health, dental, vision, HSA, FSA, and commuter reduce both income tax and FICA. A traditional 401(k) reduces income tax only, so Social Security and Medicare still apply to the full contribution amount.

Because the deduction was pre-tax. A $200 pre-tax deduction might only lower your net pay by $140 to $150, since you also stop paying tax on that $200. A $200 post-tax deduction removes the full $200 from your take-home pay.

A traditional 401(k) is pre-tax, so it lowers your taxable income now and is taxed when you withdraw it in retirement. A Roth 401(k) is post-tax, so you pay tax now and qualified withdrawals are tax-free later. Both share the same 2026 contribution limit of $24,500.

So that any benefits you receive are tax-free. If premiums are paid pre-tax, the disability payments you collect later are treated as taxable income. Since disability typically replaces only part of your salary, many people prefer the tax-free post-tax route.

Yes, and many people do. A common setup is pre-tax health insurance plus post-tax Roth 401(k) contributions. If you split between a traditional and a Roth 401(k), the combined total still cannot exceed the annual IRS contribution limit.

Starting January 1, 2026, employees age 50 and older who earned more than $150,000 in Social Security wages the previous year must make all 401(k) catch-up contributions on a Roth, post-tax basis instead of pre-tax.