What Is FICA on a Pay Stub? 2026 Rates, Wage Limit and Calculation Examples

By ePaystubs Editorial Team | Updated June 22, 2026 | Verified against IRS Topic 751

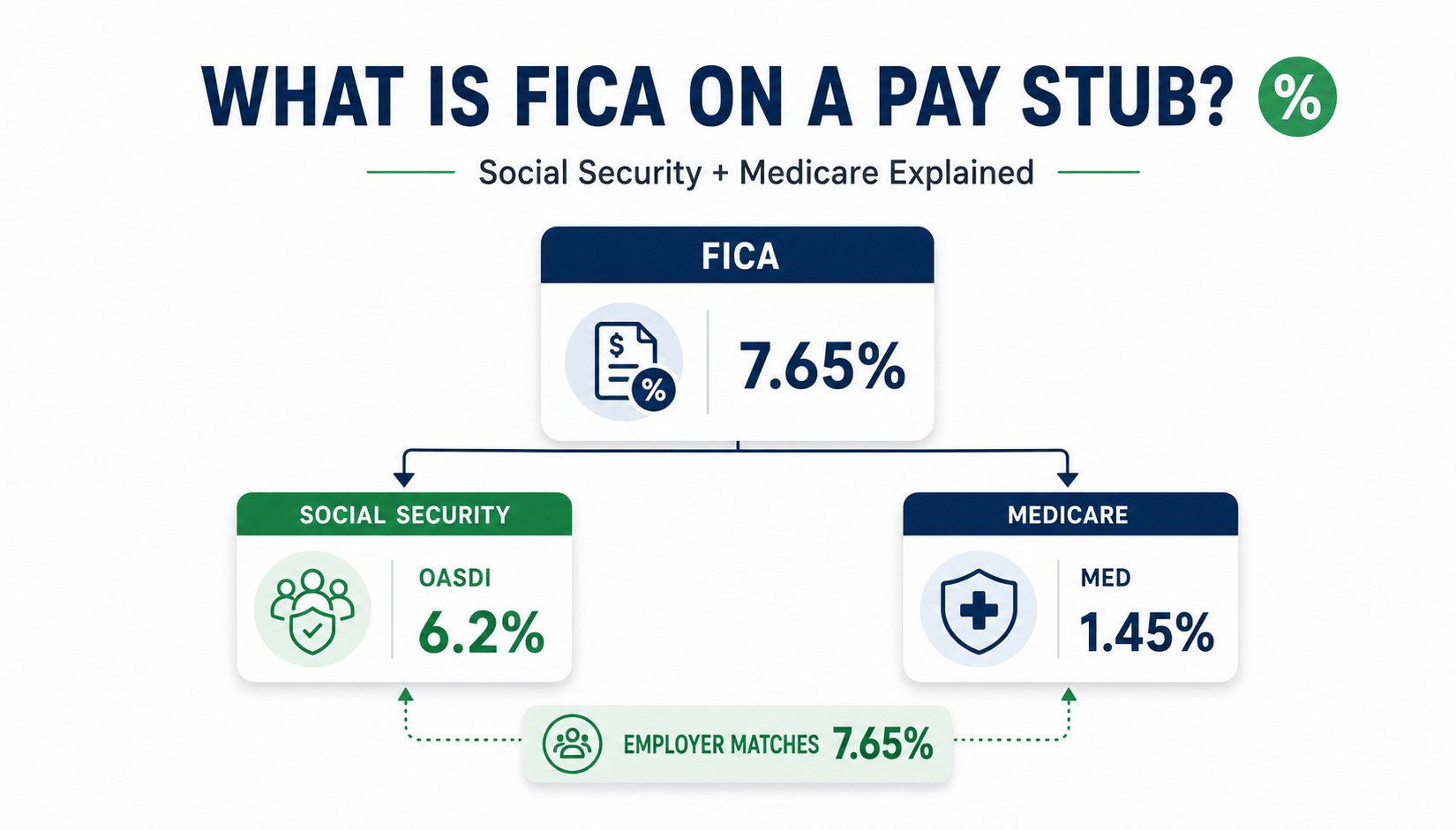

FICA stands for the Federal Insurance Contributions Act. It is a mandatory federal payroll tax that funds Social Security and Medicare. On your pay stub it appears as two lines -- one for Social Security (6.2%, labeled OASDI or FICA/SS) and one for Medicare (1.45%, labeled MED or FICA/Med). Together they equal 7.65% of your gross wages. Your employer matches that same 7.65% separately -- it never comes out of your pay.

Most workers see both lines and assume they are being charged twice. They are not. The two lines are one tax split into its two components for legal reporting purposes. This guide covers the confirmed 2026 rates, how FICA is calculated, why the stub shows two lines (and not one), what happens when Social Security withholding stops mid-year, and how FICA differs from every other deduction on the same stub.

What FICA Stands For and Why It Exists

Congress enacted the Federal Insurance Contributions Act in 1935 as part of the original Social Security Act -- a direct response to the financial devastation of the Great Depression that left elderly Americans without retirement income. The law created a payroll tax mechanism to fund Social Security, a program providing retirement income, disability benefits, and survivor benefits for qualifying workers and their families. Medicare was added in 1965 to provide hospital insurance for Americans aged 65 and older.

FICA is not a welfare program. Every dollar you pay builds eligibility toward benefits you will receive later. The Social Security Administration tracks your contributions through your Social Security Number and uses that history to calculate your eventual benefit. Pay in more over your working life and your retirement or disability benefit will be higher. Medicare Part A -- hospital coverage from age 65 -- requires at least 10 years (40 quarters) of FICA contributions to qualify at no premium cost.

Mechanically, your employer collects both the employee portion and the employer matching portion each pay period, then deposits the combined amount to the IRS electronically on a set schedule. The IRS allocates the funds to two separate federal trust funds -- the OASDI Trust Fund for Social Security and the Hospital Insurance (HI) Trust Fund for Medicare. Those separate trust funds are precisely why your stub shows two lines instead of one.

The 2026 FICA Rates (IRS-Confirmed)

The FICA rates are unchanged for 2026, but the Social Security wage base increased from $176,100 to $184,500 -- a 4.8% jump driven by the national average wage index. Here is the full breakdown, verified against IRS Topic 751 and the SSA Contribution and Benefit Base announcement:

| Component | Employee Rate | Employer Rate | 2026 Wage Cap | Max Employee Contribution |

|---|---|---|---|---|

| Social Security (OASDI) | 6.2% | 6.2% | $184,500 2026 | $11,439 |

| Medicare (HI) | 1.45% | 1.45% | No cap | No limit |

| Additional Medicare Tax | 0.9% | None (no match) | $200,000 single / $250,000 MFJ / $125,000 MFS | Varies |

| Total standard employee | 7.65% | 7.65% | -- | -- |

The Additional Medicare Tax of 0.9% applies only to wages above the threshold -- not to all wages once the threshold is crossed. A single filer earning $220,000 pays the extra 0.9% only on the $20,000 above $200,000, not on the full $220,000. The employer does not match this portion and is not liable for it, though the employer must begin withholding it once an employee's wages cross $200,000 in the calendar year regardless of the employee's actual filing status.

What Changed for 2026 Under the One Big Beautiful Bill Act

The One Big Beautiful Bill Act, signed in July 2025, permanently eliminated the income exclusion for employer-paid moving expense reimbursements for non-military employees. Previously, these reimbursements were excluded from FICA wages under a temporary TCJA-era suspension. Starting in 2026, if your employer covers relocation costs, those amounts are fully included in your FICA wage base and must appear on your W-2. This is a permanent change, not a one-year adjustment.

Why Your Pay Stub Shows Two Lines Instead of One

FICA is one tax obligation. Yet every pay stub lists it as two separate deductions. This is the most common source of FICA confusion -- workers assume they are being double-charged.

The reason is a legal reporting requirement rooted in how each program is funded. Social Security and Medicare are administered through separate federal trust funds with completely different caps, rules, and benefit structures. IRS Form 941 -- the quarterly payroll tax return every employer files -- reports Social Security taxes and Medicare taxes as distinct line items. Payroll systems mirror that same structure on the employee-facing stub.

Seeing two lines is a transparency and compliance requirement, not evidence of two separate taxes being levied. The two amounts added together equal your total FICA contribution for that pay period.

The exact label on each line depends on the payroll platform your employer uses:

| FICA Component | Common Stub Labels | Rate |

|---|---|---|

| Social Security | OASDI, FICA/SS, Fed OASDI/EE, SS Tax, SOCSEC | 6.2% |

| Medicare | MED, FICA/Med, Fed MED/EE, HI, Medicare Tax, MEDI (Workday) | 1.45% |

If you switch employers and notice a different label for the same deduction, the payroll platform changed -- not the tax itself. All labels in the Social Security row above refer to the same 6.2% deduction. All labels in the Medicare row refer to the same 1.45% deduction.

For a complete breakdown of the Social Security line -- including what OASDI stands for, the wage base history, and how your contributions build future benefit credits -- see what OASDI means on your pay stub. For the Medicare line specifically, including the Additional Medicare Tax threshold and how Medicare Part A eligibility is earned, see what MED means on a pay stub.

How FICA Is Calculated: A Worked Example

FICA math is straightforward once you have the rates and your gross pay for the period. Here is a full calculation for a salaried employee earning $55,000 per year on a biweekly schedule (26 pay periods).

| Line Item | Calculation | Per Pay Period | Full Year |

|---|---|---|---|

| Gross pay | $55,000 / 26 | $2,115.38 | $55,000.00 |

| Social Security (6.2%) | $2,115.38 x 0.062 | $131.15 | $3,410.00 |

| Medicare (1.45%) | $2,115.38 x 0.0145 | $30.67 | $797.50 |

| Total FICA (employee) | SS + MED | $161.82 | $4,207.50 |

| Employer match (not on stub) | Same as employee | $161.82 | $4,207.50 |

| Combined FICA deposited to IRS | Employee + employer | $323.64 | $8,415.00 |

At $55,000, this worker is well below the $184,500 SS wage base, so the full 7.65% applies all year. The employer's $161.82 matching contribution is a separate payroll cost -- it never reduces the employee's gross wages or appears anywhere on the pay stub.

Self-Employed? You Pay SECA Instead of FICA

Freelancers, independent contractors, and sole proprietors do not pay FICA. They pay the equivalent under the Self-Employment Contributions Act (SECA) at 15.3% of net self-employment earnings -- covering both the employee and employer halves since there is no employer to split with. Here is what that looks like for a self-employed worker netting $75,000:

SECA Calculation -- $75,000 Net Self-Employment Income

The IRS applies the 92.35% adjustment (equivalent to 1 minus the 7.65% employer share) to replicate the fact that W-2 employees only pay FICA on their take-home wages, not on the employer's matching cost. The deductible employer half reduces your adjusted gross income when you file -- it does not reduce the SECA tax itself.

What Happens When Social Security Withholding Stops Mid-Year

Social Security tax applies only to the first $184,500 of wages in a calendar year. Once your year-to-date gross wages hit that threshold, the 6.2% Social Security line stops appearing on your pay stubs for the rest of the year. Medicare continues on every dollar you earn with no cap, ever.

For a worker earning $190,000 annually on a biweekly schedule ($7,307.69 per period), the Social Security wage base is hit partway through pay period 26 -- around late December. Each paycheck after crossing $184,500 is approximately $452.77 larger (6.2% of the remaining biweekly gross) because the OASDI line disappears. On January 1, the wage base resets and withholding starts again from zero.

If you notice your FICA deduction drop mid-year, this is the most common explanation. Check your year-to-date gross wages on the stub against the $184,500 threshold. If you have reached it, the change is correct. If you have not reached it and the deduction dropped anyway, contact payroll immediately.

The Multi-Job Overpayment Problem

Workers with two or more employers face a specific wrinkle. Each employer withholds Social Security independently -- neither knows what the other is withholding. If your combined wages from both jobs exceed $184,500 in the year, you will overpay Social Security across the two payroll systems during the year. Neither employer is doing anything wrong; each is correctly withholding on the wages they pay.

The correction happens at tax filing, not during the year. You claim the excess Social Security withheld as a credit on your personal federal return. The employers do not receive a refund and are not involved. Medicare overpayment is never refundable, and if your combined income clears $200,000, the Additional Medicare Tax may also apply -- sort that out on Form 8959 at filing.

FICA vs Federal Income Tax: Key Differences

FICA and federal income tax (FIT) both appear as deductions on every pay stub, which leads many workers to treat them as versions of the same thing. They are calculated differently, fund entirely different programs, and respond to completely different inputs.

| Feature | FICA | Federal Income Tax (FIT) |

|---|---|---|

| Rate structure | Flat 7.65% | Progressive 10%--37% |

| Affected by W-4 elections? | No | Yes |

| Wage cap? | Yes -- SS stops at $184,500 | No |

| Employer match? | Yes -- full 7.65% | No |

| 2026 standard deduction reduces it? | No -- applies to all gross wages | Yes -- $16,150 single / $30,000 MFJ |

| 401(k) pre-tax deferral reduces it? | No | Yes |

| Funds | Social Security and Medicare trust funds | General government operations |

| Earns future benefits? | Yes -- retirement, disability, Medicare Part A | No direct benefit linkage |

Federal income tax withholding works through an entirely different mechanism -- W-4 elections, IRS Publication 15-T withholding tables, and progressive brackets. For a full breakdown of how the FIT line is calculated and what every label means, see what FIT or FWT means on a pay stub.

Who Pays FICA and Who Is Exempt

Nearly every W-2 employee in the United States pays FICA. It is mandatory. No W-4 election, filing status, or voluntary deduction changes that. A small number of workers are formally exempt:

| Exempt Group | Condition |

|---|---|

| Students employed by their own university | On-campus work only while enrolled; off-campus jobs are fully FICA-subject |

| Nonresident aliens on F-1, J-1, M-1, Q-1/Q-2 visas | First five calendar years of U.S. presence; exemption ends once they become resident aliens |

| Children under 18 in a parent's sole proprietorship | Exemption ends at 18; does not apply to corporations or partnerships with non-parent partners |

| Household workers earning under $3,000/year from one employer | 2026 IRS threshold per Publication 926; above $3,000, standard FICA applies |

| Certain foreign government employees | Wages paid in an official foreign government capacity per IRS guidance |

| Some religious group members | Requires formal IRS exemption with documented religious opposition to receiving benefits |

Does FICA Vary by State?

No. FICA is a federal tax and the rates are identical for every U.S. worker regardless of which state they work in. You pay 6.2% for Social Security and 1.45% for Medicare whether you are in California, Texas, Florida, or any other state.

What varies by state is state income tax -- a separate line with nothing to do with FICA. Some states also have payroll taxes such as State Disability Insurance (SDI) or State Unemployment Insurance (SUI/SUTA) that appear as additional deductions on your stub. These are entirely separate state programs. Your state page at epaystubs.net/state has the full breakdown of payroll deductions specific to where you work.

Frequently Asked Questions About FICA on a Pay Stub

No. FICA is the Federal Insurance Contributions Act -- the law that collects both Social Security (6.2%) and Medicare (1.45%). Social Security is one component of FICA, not the whole thing. When your stub shows two FICA lines, both are part of the same single tax obligation.

Yes. Your employer matches your 7.65% dollar for dollar. You see only your half on the pay stub. The employer matching contribution is a separate payroll cost on top of your gross wages and never reduces your take-home pay.

No. FICA is a flat mandatory rate. W-4 elections, deductions, and filing status have no effect on it. The only way FICA decreases mid-year is when your year-to-date wages hit the $184,500 Social Security wage base -- at that point Social Security withholding stops, though Medicare continues on every dollar earned for the rest of the year.

No. Pre-tax 401(k) deferrals reduce your federal income tax wages but not your FICA wages. FICA applies to your full gross wages before the 401(k) deduction. This surprises many workers who assume all pre-tax deductions lower every tax line on the stub.

Each employer withholds Social Security independently. If your combined wages exceed $184,500, you will overpay Social Security across both jobs. You claim the excess as a credit on your personal federal tax return at filing. The employers are not involved in the refund -- it goes directly to you from the IRS.

The IRS requires employers to track and report each FICA component separately because Social Security and Medicare are funded through separate federal trust funds with different caps and rules. IRS Form 941 reports them as distinct line items, and payroll systems follow that same structure. Two lines is a legal compliance requirement, not evidence of two separate taxes.

Your employer is violating federal law. You are still responsible for your portion of the tax. File IRS Form 8919 (Uncollected Social Security and Medicare Tax on Wages) with your return to document what was not withheld. The IRS will pursue your employer for penalties and interest, but your underlying tax obligation does not disappear.

Yes. Bonuses, commissions, tips, and other compensation are FICA wages and are subject to the same 7.65% rate as regular wages. Your employer withholds FICA from these payments exactly as they do from your regular paycheck. Tips over $20 per month must also be reported to your employer so FICA can be withheld.