Proof of Income for a Mortgage: Pay Stubs, W-2s, Tax Returns & More

By ePaystubs Editorial Team | Updated June 22, 2026

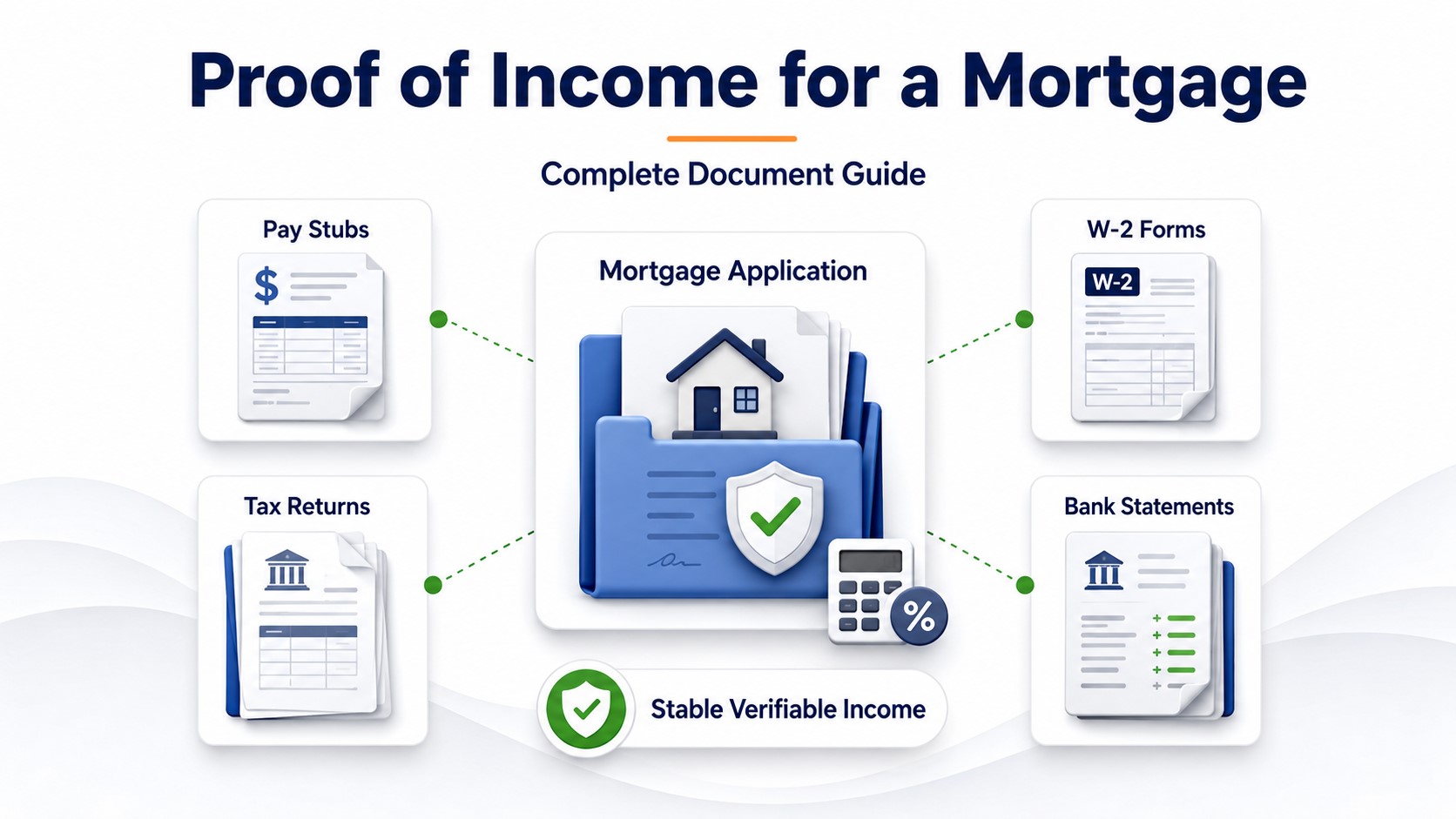

To prove your income for a mortgage, most lenders want your two most recent pay stubs, two years of W-2s, and two years of tax returns, plus authorization to pull your tax transcripts from the IRS. Bank statements verify your income and down payment. There's no minimum salary to qualify, what matters is that your income is stable, verifiable, and enough to cover the payment. This guide covers the documents, which income types count, how lenders verify them, and how much income you need.

A mortgage is a 30-year commitment, so lenders verify your income more carefully than they do for almost any other loan. That can make the paperwork feel intimidating, but it follows a predictable pattern once you know what lenders are looking for and why. This guide walks through the documents you will need, which kinds of income count toward qualifying, how lenders actually verify your earnings, and how much income it takes to afford the home you want. A mortgage sits at the demanding end of what lenders need to verify income across loan types. One note up front: we are a pay-stub resource, not a mortgage lender, so treat this as a clear explainer of how mortgage lenders think.

- What proof means

- Documents you'll need

- Which income counts

- How lenders verify

- How much income

- The two-year rule

- If you're self-employed

- Honesty and your pay stub

What Proof of Income Means for a Mortgage

Lenders are agreeing to hand over a large sum they will not be fully repaid on for decades, so they examine your income closely to confirm you can carry the payment. That is why proof of income is more involved for a mortgage than for a car loan or a credit card.

What you will need to provide depends partly on how you earn. A salaried W-2 employee has the most direct path, while self-employed and variable-income borrowers provide more, both of which this guide covers, with deeper routes where the topic warrants its own guide.

The Documents You'll Need

For a typical salaried borrower, the core document set looks like this.

- Pay stubs — your two most recent, covering at least the last 30 days and showing year-to-date earnings

- W-2s — the last two years, to establish your income history

- Tax returns — the last two years, sometimes three, especially if you have non-salary income

- IRS Form 4506-C — you sign this to let the lender pull your tax transcripts directly from the IRS as a verification backstop

- Bank statements — to verify your income deposits, your assets, and your down payment

If your income includes 1099 or contractor work, see our guide to 1099 proof of income for how that documentation works.

Which Income Types Count for a Mortgage

More kinds of income qualify than most people expect. The recurring rule is that non-salary income usually needs a two-year history and proof it will continue for at least three more years.

| Income type | The rule |

|---|---|

| Salary / hourly | The standard; pay stubs, W-2s, and tax returns |

| Commission, bonus, overtime, RSUs | Counts with a 2-year history; a one-time signing bonus does not, but annual bonuses do |

| Self-employed / business | 2 years of returns, calculated from net income (see below) |

| Rental income | Lenders typically use about 75% of market rent, not 100% |

| Dividends, interest, capital gains | Documented 2-year history and expected continuation |

| Retirement, pension, Social Security | Must be expected to continue at least 3 years past closing |

| Alimony / child support | Received 6 to 12 months, continuing 3+ years, with the court order and proof of receipt |

| Disability / benefits | Count if steady and long-term |

| Combined incomes (couples) | Both incomes count, but the lower credit score usually sets the rate |

The pattern to take away: consistency and a documented track record are what turn an income source into qualifying income. A new or one-off payment rarely counts; a steady, provable one usually does.

How Lenders Verify Your Income

Lenders do not just collect your documents, they verify both your income and your employment, often more than once during the loan. Knowing how helps you avoid the mistakes that derail applications.

The methods include reviewing your documents, calling your employer directly, using automated systems for large employers, and increasingly using digital verification that reads your payroll or bank data with your permission. Throughout, lenders cross-check your numbers across sources, your pay stubs against your W-2s against your tax returns, so the figures all need to agree.

How Much Income Do You Need? The 28/36 Rule

Since there is no minimum salary, lenders measure affordability with your debt-to-income ratio, your monthly debt payments divided by your gross monthly income. The common guideline is the 28/36 rule.

Many lenders prefer your mortgage payment to stay under about 28% of your gross income and your total debt under 36%. Worth separating two ideas here: qualifying and affording are not the same. You might qualify for a $500,000 mortgage, but that does not mean you should borrow it, the payment has to fit your real life, not just the formula. As a quick reference, credit-score minimums run roughly 620 for conventional loans, 580 for FHA (some lenders lower with more down), 580 to 620 for VA, and 640 for USDA, with jumbo loans wanting the low-to-mid 700s.

The Two-Year Stability Rule (and the Career-Change Trap)

Lenders want to see about two years of steady income with no unexplained gaps in employment. The nuance that catches people off guard is what counts as steady.

If You're Self-Employed

Self-employed borrowers, including 1099 contractors, freelancers, and business owners, can absolutely get a mortgage, but the process works differently enough to deserve its own guide. The short version: lenders want two years of tax returns and calculate your income from your net profit after deductions, not your gross, which means heavy write-offs can lower the income you qualify on.

One honest note: a "no income verification" or stated-income mortgage exists for some borrowers with high assets or irregular income, but these are specialized non-QM products, and the self-employed guide above covers when they actually make sense.

A Note on Honesty (and Your Pay Stub)

Everything on a mortgage application has to be accurate, and the stakes here are higher than on most paperwork.

If you need a pay-stub-style document for your real income, you can create a pay stub in a few minutes and present it with your application.

Frequently Asked Questions

Typically your two most recent pay stubs, two years of W-2s, and two years of tax returns, plus a signed Form 4506-C letting the lender pull your IRS transcripts. Bank statements verify your income and down payment. Self-employed borrowers provide two years of returns and additional documents.

Usually your two most recent, covering at least the last 30 days and showing year-to-date earnings. Lenders compare these against your W-2s and tax returns, so the figures need to line up across all three.

No. There's no set minimum salary. Lenders care whether your income is stable, verifiable, and enough to cover the payment given your other debts. Two people with the same income can qualify for very different amounts depending on their existing debt.

Many types: commission, bonus, and overtime with a two-year history; rental income at about 75% of market rent; dividends and interest with a documented history; and retirement, Social Security, alimony, or child support that will continue at least three years. Most non-salary income needs a track record.

They review your documents, often call your employer, sometimes use digital verification of payroll or bank data, and cross-check your pay stubs against your W-2s and tax returns. They usually re-verify right before closing, so avoid changing jobs during the process.

A common affordability guideline: your mortgage payment should stay under about 28% of your gross monthly income, and your total debt payments under 36%. It's why lenders focus on your debt-to-income ratio rather than a minimum salary.

Yes, but the process differs. Lenders want two years of tax returns and use your net income after deductions, so heavy write-offs can lower your qualifying income. See our guide on self-employed mortgage income for the full picture, including the income math and loan options.