Proof of Income When Self-Employed: Tax Returns, 1099s & Bank Statements

By ePaystubs Editorial Team | Updated June 22, 2026 | Tax details verified against the IRS Self-Employed Tax Center

When you're self-employed, proving your income takes more than a pay stub, because no employer withholds your taxes or hands you a W-2. You become the record-keeper. The documents that carry the most weight are your tax returns and bank statements, supported by 1099s, profit and loss statements, and invoices. Which combination you need depends on what you're applying for. This guide covers the full toolkit, how to organize it by situation, and the tax basics every self-employed person should know.

Working for yourself comes with real freedom, and one real headache: the moment a landlord, lender, or agency asks you to prove what you earn. There is no HR department to call and no pay stub to hand over. The good news is that proving self-employed income is a solvable, well-understood problem. Every major lender, landlord, and agency has a process for it. You just need to know which documents count, how to organize them, and which ones to lead with for your specific situation. This guide is the map, and it points you to deeper guides for the situations that need them. For how income proof works across every earner type, not just the self-employed, see our overview of proving proof of income generally.

- Why it's different

- Self-employed and tax basics

- The net-vs-gross gap

- The document toolkit

- Documents for your situation

- Build the habit

- A note on pay stubs

Why Proving Self-Employed Income Is Different

A salaried worker has an employer who withholds taxes, issues a W-2 each January, and confirms employment when a landlord calls. A self-employed person has none of that. No one withholds your taxes, no one issues you a W-2, and no one is standing by to verify your income. That responsibility shifts to you, which means you assemble the documentation yourself.

In the eyes of the IRS and a lender, being self-employed simply means you run your own business with no employer withholding your taxes, whether you are a freelancer, an independent contractor, a gig worker, a sole proprietor, or a business owner. The challenge that follows is not a lack of proof, it is knowing which documents to present, how to organize them, and how to match them to what a specific lender, landlord, or agency actually wants. That is an organization problem, not an impossible one, and the rest of this guide solves it.

What Counts as Self-Employed (and the Tax Basics to Know)

You are self-employed if you work for yourself rather than an employer: you own a business, freelance, contract, or do gig work. A few tax basics are worth knowing up front, because your tax situation shapes your strongest proof of income.

Two forms do the work: Schedule C reports your business profit or loss, and Schedule SE computes your self-employment tax. Both attach to your Form 1040. This matters for proof of income because that filed return, the one built from your Schedule C, becomes your single most credible income document.

The Gap Between What You Earn and What Your Documents Show

Here is a dynamic that trips up nearly every self-employed applicant: business deductions lower your taxable income, so the number on your tax return is your net, not what you actually brought in.

To a lender or landlord reading that return, the income looks like $53,000, not $65,000. Understanding this gap is the key to presenting your income well, because it shapes which documents you lead with.

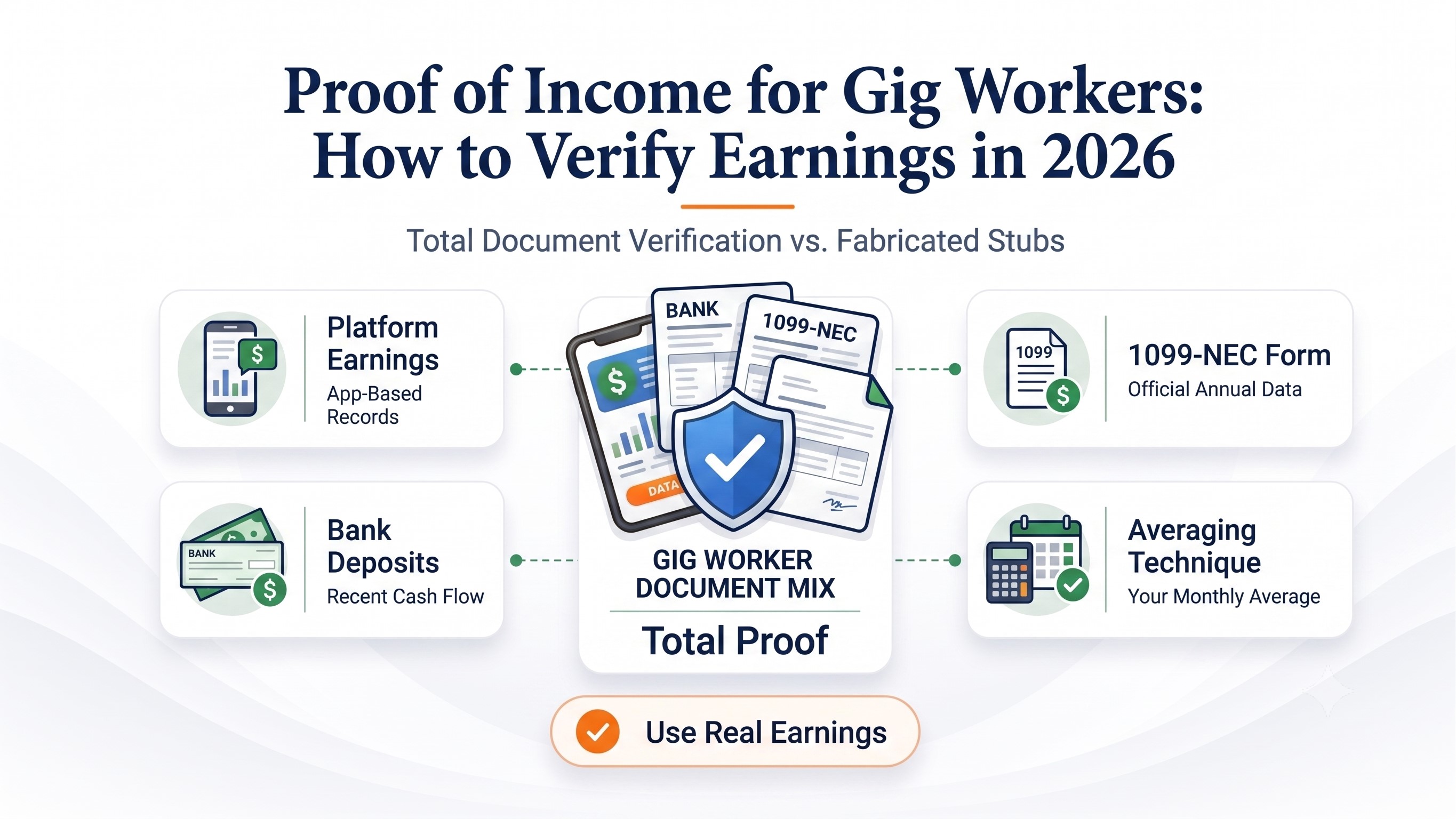

The Self-Employed Proof-of-Income Toolkit

These are the documents self-employed people use to prove income, roughly in order of how much weight they carry. You rarely need all of them, the right combination depends on your situation, which the next section covers.

1 Tax returns (Form 1040 + Schedule C)

The gold standard. Nothing carries more weight with a lender than a filed federal tax return, because it is an official IRS document. Expect to provide two years for serious applications like a mortgage. Remember it shows your net income after deductions.

2 Bank statements

Where a tax return is historical, bank statements show your current, real-time cash flow, exactly what a landlord or lender wants to see. Keep a business account separate from personal so your deposits are clear. Two to three months is typical.

3 1099 forms

Third-party verification from the clients who paid you, which makes them more credible than self-reported figures. The 1099 is a deep topic of its own, including the threshold changes taking effect in 2026.

4 Profit and loss statement

A snapshot of your business performance over a period, summarizing revenue, costs, and net profit. It carries more weight when prepared or reviewed by a CPA, and it fills the gap between annual tax returns.

5 CPA or tax-preparer letter

A licensed professional vouching for your income carries real weight, because they are staking their reputation on it. An excellent supplement, especially for nuanced situations like recent growth, seasonal income, or a move from part-time to full-time self-employment.

6 Invoices and contracts

A paper trail tying your income to specific work for specific clients. Powerful supporting documents that corroborate your other records, though they are rarely accepted on their own.

7 A self-made pay stub

A way to present your real income in a familiar format, useful as a supporting piece alongside the verifiable documents above. More on using these honestly below.

Which Documents You Need for Your Situation

The right documents depend on what you are applying for. Find your situation below and head to the guide that covers it in depth.

Buying a home

The most demanding: two years of returns, your net qualifying income, and more.

You're a 1099 contractor

Your 1099s plus the right supporting documents, and the 2026 threshold changes.

You're paid in cash

The special challenge of no automatic paper trail, and how to build one.

Gig or platform work

Platform-specific records for Uber, DoorDash, Instacart, and more.

Renting an apartment

Usually lighter: returns or 1099s plus a few months of bank statements.

Benefits or health coverage

Agencies like Covered California and Social Security publish their own accepted-document lists, often your latest return with Schedule C and SE, or a P&L.

You need a written letter

A template you can adapt for a landlord or lender.

Build the Habit: Proof Starts Before Anyone Asks

The self-employed people who never stress about proof of income are not the ones with special documents, they are the ones who keep clean records all year. Proving your income is a scramble only when you have not been tracking it. When you have, your proof assembles itself.

The habits are simple: keep a business account separate from your personal one, log your income and expenses (a spreadsheet works, or accounting software), update it regularly, and keep your numbers consistent across documents. When your tax return, your bank statements, and your ledger all agree, a reviewer trusts the figure immediately. To see how your income adds up across the year, see our guide on how to track your year-to-date earnings.

A Note on Self-Made Pay Stubs

You can format your real self-employed income into a pay stub to present it in a familiar format, as one supporting piece alongside your verifiable documents, never as a replacement for them.

If you need a pay-stub-style document for your real income, you can create a pay stub in a few minutes and present it alongside your tax return and bank statements.

Frequently Asked Questions

Lead with your tax returns and bank statements, the two documents that carry the most weight, and support them with 1099s, a profit and loss statement, and invoices as needed. Which combination you need depends on what you're applying for, with mortgages requiring the most and rentals usually less.

A filed federal tax return (Form 1040 with Schedule C) is the gold standard, because it's an official IRS document. Pair it with bank statements showing your deposits, since returns show historical income while statements show current cash flow. Together they're the strongest combination.

Yes, and they're one of the strongest documents you have, because they show real money flowing into your accounts. Keep a business account separate from personal so the deposits are clear, and expect to provide two to three months. They work best alongside your tax return.

For a mortgage, usually yes, lenders typically want two years to confirm stability. For an apartment or many other purposes, one year of returns plus bank statements is often enough. The more significant the application, the more history you'll generally need.

Self-employment tax is 15.3%, which is 12.4% for Social Security and 2.9% for Medicare. For 2026, the Social Security portion applies to the first $184,500 of net earnings, and the Medicare portion has no cap. You owe it once your net self-employment earnings reach $400.

This is common, because deductions lower your taxable income and 1099s only cover payments of $600 or more. Supplement your return with bank statements that show all your deposits, and consider a profit and loss statement, so the fuller picture of your income is visible.

You can create documents like a pay stub or a profit and loss statement from your real figures to present your income clearly, as long as they reflect what you actually earned and match your tax return and deposits. They work as supporting documents, not as replacements for your verifiable records.