Proof of Income for a Car Loan: When You Need It and What Works

By ePaystubs Editorial Team | Updated June 22, 2026

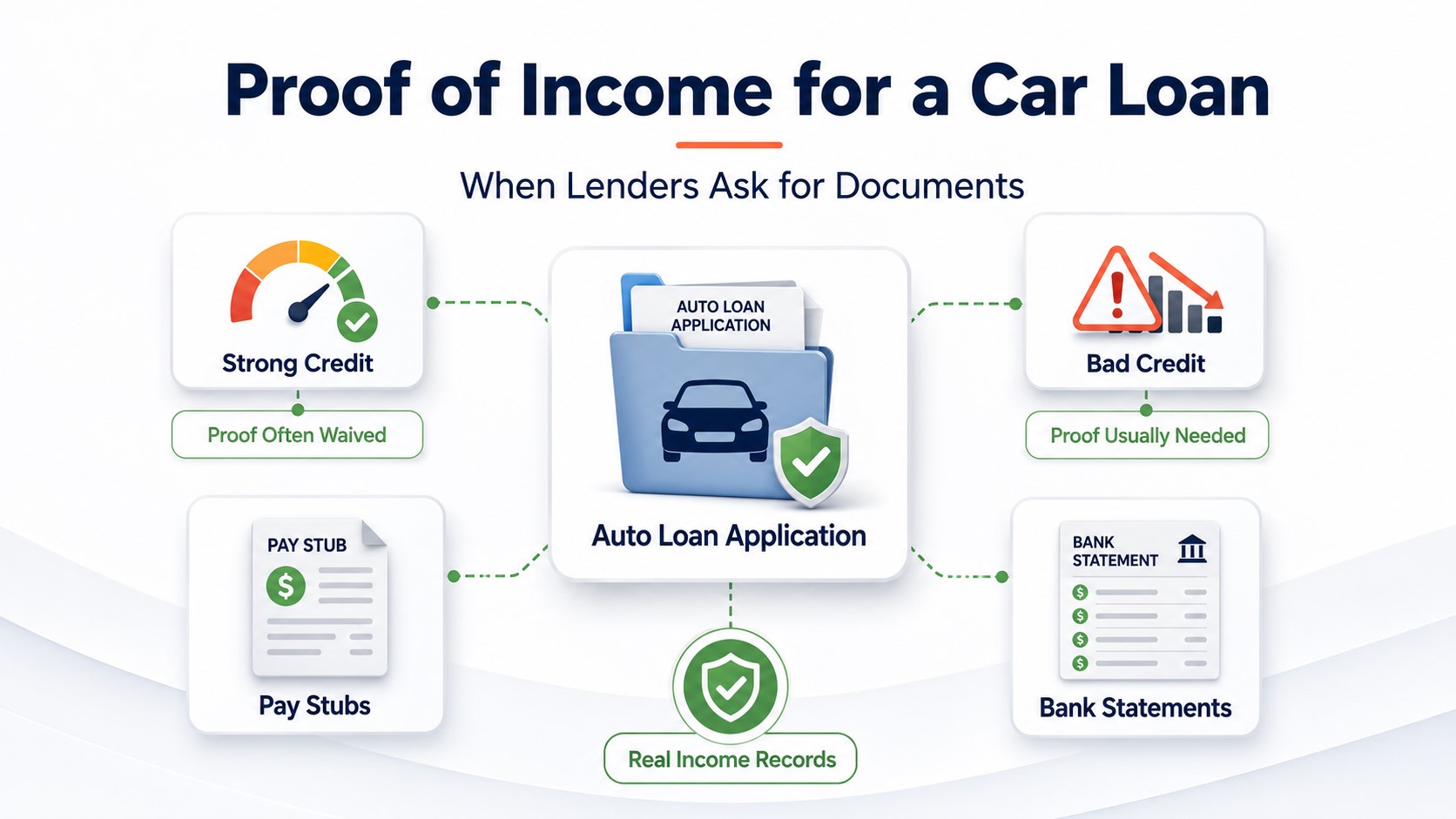

Whether you need to prove income for a car loan depends mostly on your credit. With strong credit or a large down payment, many lenders will approve you without income documents. With bad credit, a non-standard job, or an expensive car, expect to provide proof, usually recent pay stubs, bank statements, W-2s, or tax returns. This guide covers when proof is required, which documents work, the minimum income lenders look for, and the path for bad-credit borrowers.

A car loan is one of the few major loans where you might not have to prove your income at all. Unlike a mortgage, which always verifies income, an auto lender's request for proof depends on how much risk they see in you, so the first real question is not "what documents do I need," but "am I even in the group that has to prove it?" This guide answers that, then covers the documents that work, how much income lenders want to see, and what changes with bad credit. For the bigger picture across every loan type, see our overview of proof of income for a loan. One note up front: we are a pay-stub resource, not an auto lender, so treat this as a clear explainer of how auto lenders think.

- Do you even need proof

- The quick decision

- When you don't

- When you do

- Documents that work

- How much income

- Bad credit and BHPH

- The car-buying process

Do You Even Need to Prove Income for a Car Loan?

Here is what makes a car loan different from a home loan: a mortgage always verifies your income, but an auto loan often does not. Whether a lender asks for proof comes down to how much risk they see, and the lower your risk, the less they ask.

Three things reduce or eliminate the need for income documents: a strong credit score, a large down payment, and a stable, easy-to-verify job. A borrower with good credit and a clean history may be approved on their stated income alone, while a borrower with weak credit will almost always be asked for documents. So the real question is not which proof you need, it is whether you are in the group that has to provide it, which the next two sections sort out.

When You DON'T Need Proof of Income

Lenders often skip income verification in these cases:

Proof often waived

Lower-risk borrowers

- Strong credit (roughly 670 or higher) with a clean payment history

- A large down payment that lowers the lender's risk

- A stable, easily verified job and address that match your credit report

Costs more

No-income-verification loans

- A real product for high-credit borrowers or those with strong assets

- Typically higher rates, often 10% or more

- Usually a larger down payment and stricter terms

One thing to keep in mind: even when a lender does not ask for documents, you will still declare your annual pre-tax income on the application. The difference is simply whether they ask you to back that number up with paperwork.

When You DO Need Proof of Income

Expect to provide documentation in any of these situations:

| Situation | Why proof is needed |

|---|---|

| Bad or limited credit | The most common trigger; the lender leans on income to judge affordability |

| Self-employed or 1099 | Harder to verify, so documentation is expected |

| New job or short tenure | Lenders prefer 6 to 12 months in the same job or field |

| Part-time or seasonal | Usually needs 3 to 6 months of consistent history plus backup |

| An expensive car | The larger payment raises risk regardless of credit |

If your income is self-employed or comes from 1099 work, the documents follow the same principles as any self-employed income, see our guides to 1099 proof of income and, for how lenders read self-employed income closely, self-employed mortgage income. Needing to provide proof is not a problem, it just means gathering a document or two before you apply.

The Documents That Work

Auto lenders are fairly flexible about what they accept. Any of these can serve as proof of income.

| Document | What it shows |

|---|---|

| Pay stubs | The default; your most recent, sometimes 2-3 months, showing year-to-date income |

| Bank statements | 2-3 months of regular deposits; often pulled directly via secure tools like Plaid |

| W-2s | Your prior-year wages |

| Tax returns | Two years if you're self-employed |

| 1099s | For independent contractors and freelancers |

| Alternative income | Social Security, disability, pension, 1099-Rs, alimony, child support, steady side-hustle income |

If your income is self-employed, 1099, or cash-based, how you document it follows the same approach as any self-employed income, see our overview of proof of income when self-employed.

How Much Income Do You Need?

Beyond which documents to bring, lenders look at whether your income is enough to carry the payment. A few concrete benchmarks.

Lenders also look at two ratios. Debt-to-income (DTI) is the share of your monthly pre-tax income that goes to debt payments, and auto lenders generally prefer 50% or less. Payment-to-income (PTI) is the car-specific one, your car payment as a percentage of your income, which lenders watch closely. As a budgeting guideline, the 20/4/10 rule suggests putting 20% down, keeping the term to 4 years or less, and keeping total vehicle costs under 10% of your gross income.

The detail people miss is that the 10% figure is meant to cover the whole cost of the car, not just the loan payment. On $4,000 a month, that is about $400 for the payment, insurance, and fuel combined, which usually means a loan payment closer to $250 to $300 once insurance and gas are accounted for. Running this math before you shop keeps you from qualifying for a payment that looks fine on paper but squeezes your budget once the other costs land.

These thresholds are not arbitrary hurdles. They are the lender confirming you can afford the payment without stretching too thin, which also protects you from ending up in a repossession.

Getting a Car Loan with Bad Credit

If your credit is weak, the path looks different, and this is how a large share of auto loans actually work. Bad-credit (subprime) lenders almost always require proof of income, and they ask for more besides.

- A down payment, often around $1,000 or 10% of the price

- Employment history, usually at least 6 months

- A list of personal references

- Proof of residence

Buy-here-pay-here dealers finance in-house and have flexible credit requirements, but they lean heavily on income proof because they are taking the risk directly. If you are on the edge of qualifying, a larger down payment or a creditworthy cosigner can tip the decision your way.

How Income Fits the Car-Buying Process

Income comes up at three points, and knowing when helps you prepare.

- Prequalification. A preliminary check that gives a rough idea of what you might qualify for. You may only need to provide estimated income.

- Preapproval. A more involved step that produces a real offer. This usually requires income verified by documents like pay stubs.

- Finalizing. After you choose the car, the lender does a last income-verification round before the loan closes.

Getting your income documents ready before you start shopping makes every stage faster, and walking onto the lot already preapproved lets you negotiate from a stronger position.

When You Need a Pay Stub for Your Application

If a lender asks for a pay stub and you need to present your real income in that format, you can create one to provide alongside your other documents.

If you need a pay-stub-style document for your real income, you can create a pay stub in a few minutes and present it with your application.

Frequently Asked Questions

Not always. With strong credit or a large down payment, many lenders approve a car loan on your stated income without documents. With bad credit, a non-standard job, or an expensive car, you'll usually need to provide proof like pay stubs, bank statements, or tax returns.

Usually your most recent pay stub, ideally one showing year-to-date income, though some lenders ask for two or three months. If your income varies or you're self-employed, expect to add bank statements or two years of tax returns.

Subprime and bad-credit lenders typically want $1,500 to $2,500 a month before taxes from a single job. You generally can't combine two jobs to meet that minimum, one job has to clear it, though a second job can count toward your debt ratios afterward.

Yes, if you have strong credit, a large down payment, or a creditworthy cosigner. No-income-verification car loans exist for high-credit borrowers, but they carry higher rates and stricter terms. You'll still declare your income on the application even if you don't document it.

Generally no, because unemployment benefits are temporary, lenders usually won't count them. If you're between jobs, you'll typically need another income source like Social Security, disability, or a pension, or a cosigner with verifiable income.

Yes, but expect to provide more documentation, usually two years of tax returns, bank statements, and possibly 1099s, since you don't have pay stubs. Strong credit and a solid down payment make it easier. See our guide on proof of income when self-employed for how lenders read that income.

Yes. The more expensive the car, the more likely the lender asks for income verification, because the monthly payment is higher. An expensive or luxury car can trigger proof even when your credit is excellent.