Proof of Income for Gig Workers: How to Verify App Earnings

By ePaystubs Editorial Team | Updated June 22, 2026 | Tax details verified against the IRS Gig Economy Tax Center

Gig workers prove income with a combination of documents rather than a single pay stub: platform earnings records, 1099 forms, bank statements showing deposits, tax returns with Schedule C, and income verification letters. The trick is presenting variable, multi-platform income in a form lenders and landlords recognize, which usually means leading with a monthly average and backing it with a year of history. This guide covers the full document mix, the platform-by-platform specifics, and how to combine income from several apps.

If you drive for Uber, deliver for DoorDash, shop for Instacart, or pick up work through any other platform, you already know the problem: you are earning a real income, but you do not have an employer to call or a W-2 to hand over. The good news is that gig platforms produce detailed, verifiable records, and once you know which documents to use and how to present them, proving your income is more manageable than it looks. This guide is the overview, with links to step-by-step guides for each major platform. For the full proof of income picture beyond gig work, see our guide on how to show proof of income.

- The challenge

- Lead with your average

- The document mix

- By platform

- Combining platforms

- What reviewers want

- Gross vs net

- Keep it honest

Why Proving Gig Income Is Harder (and How to Fix It)

Traditional income verification was built around a simple model: one employer, one salary, one W-2 at the end of the year. Gig work does not fit that model. Your income arrives in uneven amounts from one or more platforms, with no single employer to confirm it, so an automated underwriting system often flags the file as higher risk, sometimes even when a gig worker earns more than a salaried peer.

The fix is not to pretend you are a W-2 employee. It is to translate your real income into the documents that lenders and landlords already recognize. That is the whole game, and the rest of this guide is about doing it well: which documents to use, how to present variable income credibly, and where each platform keeps your records.

Lead With Your Monthly Average

This is the single most useful technique for presenting gig income, and most people skip it. A reviewer expects a predictable monthly number, but your earnings naturally rise and fall week to week. Rather than handing over a confusing run of uneven figures, calculate a monthly average and lead with that.

Why it works: it answers the reviewer's real question, which is whether your income is stable and sufficient, instead of forcing them to interpret a pattern that looks inconsistent on paper. Back the number with your records so they can see the math is accurate. When applying for a lease or loan, bring at least 12 months of earnings history; the longer the period, the more convincingly it shows your income is real and sustainable. To understand how your running totals build across the year, see our guide on how to track your year-to-date earnings.

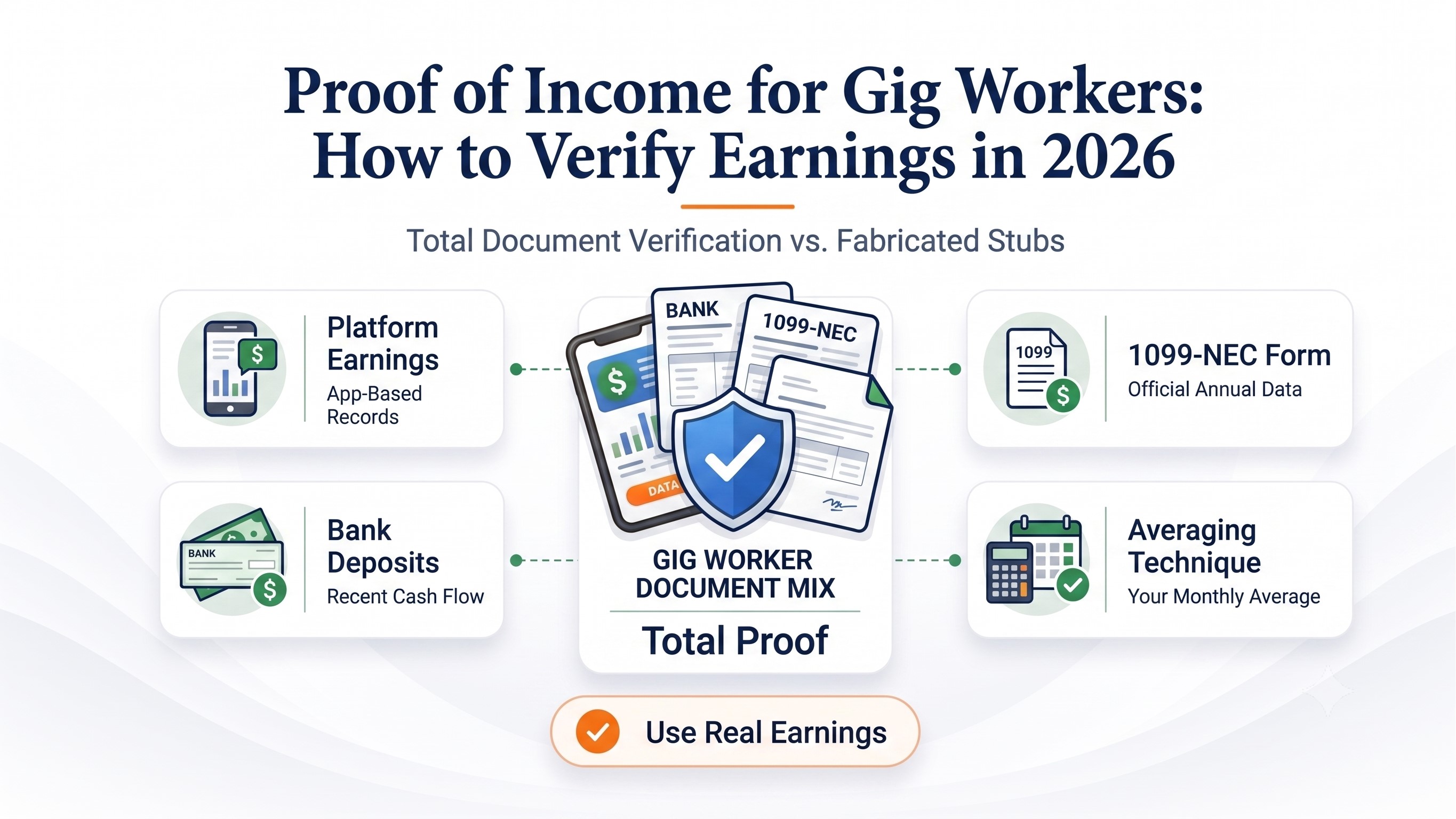

The Gig Worker Document Mix

There is no single document that works the way a W-2 does, but several combine into a strong case. Here are the widely accepted formats and what each one is best for.

| Document | What it proves | Best for |

|---|---|---|

| Platform earnings records | Current income from each app | Recent income, all applications |

| 1099 forms (NEC or K) | Official annual earnings | Tax filing, loan backup |

| Bank statements (3 to 6 months) | Deposits actually received | Rentals, proof of real cash flow |

| Tax returns with Schedule C | Reported annual net income | Mortgages, large loans |

| Income verification letter or P&L | A professional income summary | Rentals, a clean written figure |

The strongest package usually pairs a current record (earnings records or recent bank statements) with an official one (a 1099 or tax return). For how 1099 income works in detail, see our guide to 1099 proof of income. If you run your gig work as a business with expenses, our guide to proof of income when self-employed covers profit and loss statements and tax returns in depth, and you can put a clean figure in writing with an income verification letter.

Proof of Income by Platform

The exact records you pull depend on your platform, since each one stores earnings and tax documents a little differently. Here is a quick orientation for the three biggest, with a full step-by-step guide for each.

Combining Income From Multiple Platforms

Plenty of gig workers run two or three apps at once, and combining that income correctly matters both for taxes and for proof of income.

For taxes, all of your gig income from every platform goes on a single Schedule C. You report it together as one business and claim your deductions once, rather than splitting them across separate forms for each app. For proof of income, add up your monthly average across every platform to get the aggregate figure a reviewer wants. If Uber, DoorDash, and Instacart together brought in $42,000 last year, you lead with the combined $3,500 monthly average, not three separate smaller numbers.

What Each Reviewer Actually Wants

Different reviewers look for different things, and tailoring your documents to the application saves a lot of back-and-forth.

| Reviewer | What they want to see |

|---|---|

| Landlords | Aggregate income around 2.5 to 3 times the rent, plus recent deposits. A verification letter and 2 to 3 months of bank statements is a strong package. |

| Mortgage lenders | Net income after Schedule C deductions, and usually 2 years of tax returns. |

| Auto and personal loans | Active platform status and recent earnings. Some lenders now connect to your bank to verify deposits directly. |

| Credit cards | Stated income plus credit data, increasingly with bank-connected verification. |

One 2026 development worth knowing: bank-connect underwriting has gone mainstream for personal loans and buy-now-pay-later products. Instead of asking for tax returns, some lenders connect to your bank account and approve you based on a few months of steady gig deposits. Watch for a "connect your bank to verify income" option during an application, since it can be the fastest path for a gig worker. For a deeper look at specific applications, our guides on proof of income for an apartment and for a loan cover what each one needs.

Gross vs Net: Label Your Income Clearly

A small distinction causes a lot of confusion. Gross income is what you earned before expenses. Net income is what is left after fuel, maintenance, phone, supplies, and platform fees. The gap can be large, and different reviewers care about different sides of it.

Landlords tend to focus on your recent deposits and overall cash flow, closer to gross. Mortgage lenders focus on your net income after the deductions you claim on Schedule C, which can make your income look lower than your gross earnings suggest. The safe approach is to clearly label whether a figure is gross or net, and make sure the number matches the documents you submit. Mismatched figures are the fastest way to slow an application down.

Keep It Honest (and Why It Matters More Now)

Landlords and property managers actively screen for income fraud, and they are good at it. The common red flags are deposits that do not match the stated income, sudden unexplained drops, and documents that conflict with each other. Presenting your real income, clearly and consistently across every document, is not just the right thing to do, it is what gets applications approved.

If a reviewer wants a familiar pay-stub format, you can take your real aggregate earnings and format them into one, used as a supplement to your official records rather than a replacement for them. The figures must reflect what you actually earned, which your bank deposits, earnings records, and tax forms can confirm. Inventing or inflating income is fraud, and because it has to match documents a reviewer can cross-check, it is easily caught. For the full picture of what is and is not allowed, see our guide on whether it is legal to make your own pay stub.

If a landlord or lender has asked you for a pay-stub-style document, you can format your earnings into a pay stub from your real gig income in a few minutes.

Frequently Asked Questions

With a combination of documents: platform earnings records, 1099 forms, bank statements showing deposits, tax returns with Schedule C, and income verification letters. The strongest approach leads with a monthly average across all platforms and backs it with at least a year of earnings history.

It depends on the application. For rentals, a verification letter plus 2 to 3 months of bank statements works well. For mortgages, lenders want 2 years of tax returns and your Schedule C net income. For most other uses, recent platform earnings records and your 1099 are enough.

Divide your annual gross earnings by 12. If you earned $42,000 across all platforms last year, your monthly average is $3,500. Use that figure on applications and back it up with your earnings history so the reviewer can see the calculation is accurate.

Yes. For taxes, all your gig income goes on one Schedule C. For proof of income, add your monthly averages across platforms for the aggregate figure reviewers want. A single bank account used only for gig deposits makes combined income easy to show.

Most gig workers are independent contractors and receive a 1099, a 1099-NEC or 1099-K, rather than a W-2. Some roles, such as Instacart In-Store Shoppers, are employees and do get a W-2. You must report all gig income even if you receive no form.

Yes, many landlords accept gig workers who provide clear proof of income. Lead with your monthly average, show recent bank deposits, and include a verification letter or 1099. Telling the landlord up front that you're an independent contractor helps them know what to expect.

Yes. The $600 threshold only decides whether a platform sends you a 1099. You are legally required to report all gig income on your tax return regardless of whether you receive a form.