How to Prove Income Without Pay Stubs: Best Documents to Use

By ePaystubs Editorial Team | Updated June 22, 2026

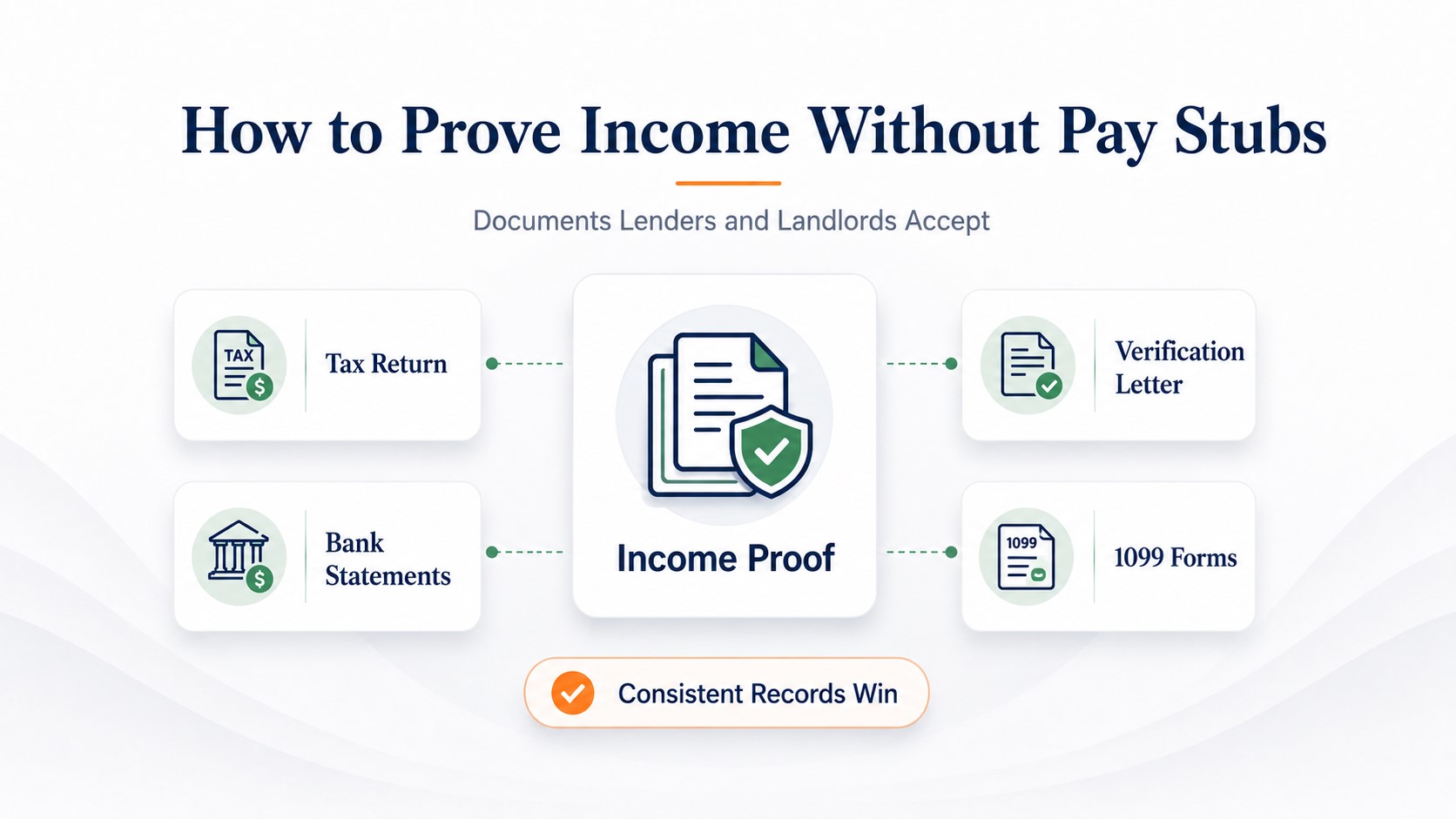

No pay stubs is not a dead end. Lenders and landlords accept tax returns, bank statements, 1099s, profit-and-loss statements, employer verification letters, offer letters, and benefit award letters as proof of income. The key isn't finding one perfect replacement, it's combining two or three documents that point to the same income figure and tell one consistent story. This guide covers every alternative that works, how each is weighted, and which combination fits your situation, whether you're self-employed, between jobs, or your employer simply doesn't issue stubs.

A pay stub is the default proof of income, but plenty of people don't have one, the self-employed, freelancers, gig workers, cash earners, the newly hired, and anyone whose employer just doesn't issue them. If that's you, the good news is that proving your income is very doable; it just takes a little more organization. We're a pay-stub resource, and we'll be straight with you: for most people without stubs, the real answer is the documents below, not a generated stub. Here's the full menu of what works, and how to put it together convincingly.

The Key Idea: Build a Case, Don't Find One Document

Most people search for the one document that replaces a pay stub. That's the wrong approach, and fixing it makes everything else easier.

A pay stub is trusted because it's an official, regular record of your earnings. You don't replicate that trust with a single substitute. You replicate it with two or three documents that corroborate each other.

Lenders and landlords want a story, not a snapshot. One document is a snapshot. Several documents that agree are a story, and a story is what earns trust.

Here's why it works. When your tax return, your bank deposits, and your 1099 all point to roughly the same income, the reviewer can trust the number, no single document could carry that weight alone. Gig workers know this instinctively; surveys find most rely on three or more documents to verify their income. The rest of this guide is the menu of what works, how each document is weighted, and which combination fits your situation.

The Documents That Work (and How Each Is Weighted)

Here is the full menu. What matters isn't just whether a document is accepted, but how much weight it carries, so each is rated below.

| Document | What it proves | How it's weighted |

|---|---|---|

| Tax return (1040 + Schedule C) | A full year of all income | Anchor |

| Bank statements | Real deposits and cash flow | Strong corroborator |

| 1099 forms | Contractor, gig, or other income | Strong |

| Profit & loss statement | Business revenue and net income | Strong (business owners) |

| Verification letter | Job, salary, status (third-party) | Strong |

| Offer letter | A new job before stubs arrive | Good |

| W-2 | Last year's wages | Supplemental |

| Invoices + contracts | Freelance earning capacity | Supporting |

| Benefit / award letters | Social Security, disability, pension, unemployment | Strong (benefit income) |

| Payment apps (PayPal/Venmo) | Transaction history | Not standalone |

| Self-attestation / affidavit | A signed statement of income | Last resort |

Think of these in three tiers. The anchor is your tax return, the most authoritative single document. The strong corroborators, bank statements, 1099s, a P&L, and verification letters, are what you build around it. And the supporting or not-standalone items, W-2s, invoices, payment apps, and affidavits, help only when paired with the stronger documents.

Which Documents Fit Your Situation

The right combination depends on who you are. Find your situation below, with the dedicated guide for the full detail.

Whichever situation fits, this is also where proof of income for a specific goal comes in, see proof of income for an apartment or proof of income for a loan for what each reviewer looks for.

How to Make Your Documents Count

Having the documents is half the job. Presenting them well is the other half. These tactics turn a pile of paperwork into convincing proof.

- Label your income deposits. On a bank statement full of transactions, highlight or annotate the ones that are income, so the reviewer can find your earnings at a glance instead of hunting for them.

- Make your documents match. The deposits on your bank statement should line up with your invoices and your tax return. Matching numbers across documents build trust; mismatches kill it.

- Show enough history. Two to three months of bank statements is a minimum. For irregular or self-employment income, aim for 6 to 12 months so your true average is clear.

- Request letters early. Verification letters from an employer, accountant, or agency take time to produce. Ask before you need them, not the day the application is due.

- Keep tax documents organized. Your most recent return is your anchor document. Have it ready, and know where your Schedule C and 1099s are.

A Note on Honesty (and Your Pay Stub)

For most people without pay stubs, the documents above are the answer. They're free, official, and carry no risk. That is honestly the best path.

There is one narrow, honest place a pay stub fits. If you have real income but no formatted stub, you're self-employed, a contractor, or paid in cash, you can put that real income into a pay stub as one document in your corroborating set. It works only if the figures are true and match your other records, your bank deposits and your tax return.

The Bottom Line

You don't replace a pay stub with one document, you build a corroborating case with two or three that agree. Tax returns and bank statements are the backbone; add the documents that fit your situation, and make sure the numbers match across all of them.

If part of your case is real self-employment or cash income that you'd like in a familiar format, a pay stub from your real earnings can be one piece of that set, sitting alongside the bank deposits and tax records that confirm it.

Frequently Asked Questions

Combine two or three documents that point to the same income: most commonly tax returns, bank statements, and 1099s. Lenders and landlords also accept profit-and-loss statements, employer verification letters, offer letters, and benefit award letters. The goal is a consistent story across documents, not one perfect replacement.

A corroborating package: your tax returns (1040 with Schedule C) as the anchor, several months of bank statements showing deposits, your 1099s, and a profit-and-loss statement. Lenders want to see income that's consistent and traceable across all of them. See our guide on proof of income when self-employed for the full approach.

Yes, bank statements are one of the most widely accepted alternatives, especially when they show consistent deposits. Label or highlight your income deposits so they're easy to find, and make sure they match your other documents. Most reviewers want 2 to 3 months, or 6 to 12 for irregular income.

A tax return is the most authoritative single document, but reviewers usually want it paired with recent proof, like bank statements, since a return only shows last year. The combination of a tax return plus current deposits is one of the strongest cases you can make.

Not on their own. Payment app history can support your case, but it's generally not accepted as standalone proof. Pair it with bank statements and invoices that show the same income, and keep a detailed transaction history.

First, request a formal income verification letter, that's the most direct fix, confirming your job, salary, and status. You can also use your W-2, bank statements showing your deposits, and your tax return. See our income verification letter guide for what to ask for.

Benefit income counts. Use your Social Security or disability award letter, an unemployment benefits letter, or a pension statement (1099-R), each showing the amount and frequency. See our guide on proof of income from government benefits for the details.