What Does YTD Mean on a Pay Stub? Earnings, Deductions and Calculation Guide

By ePaystubs Editorial Team | Updated June 22, 2026 | Verified against IRS Topic 751

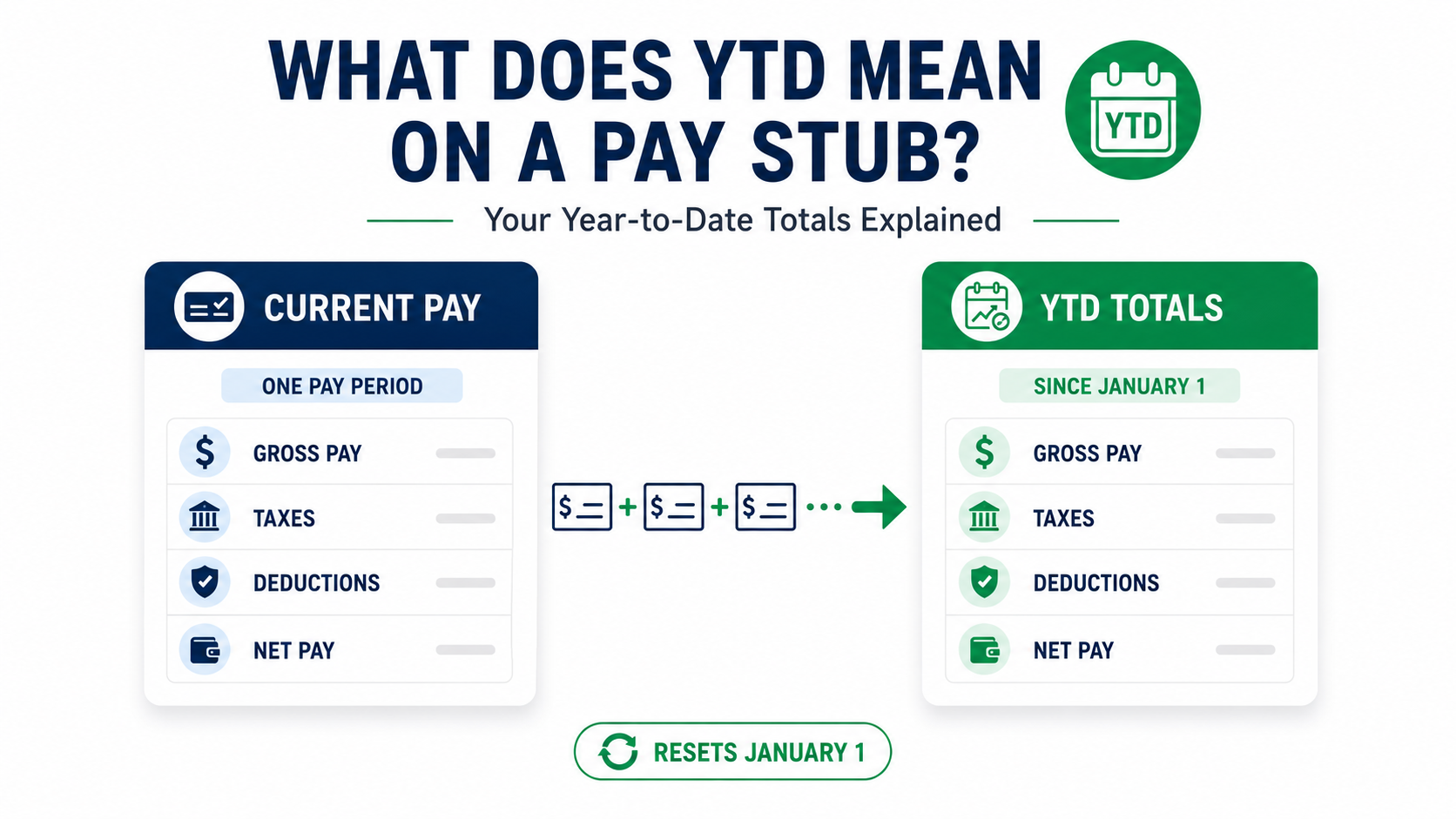

YTD stands for year-to-date. On a pay stub it is the running total of a figure -- gross pay, taxes, deductions, or net pay -- from January 1 through your most recent paycheck. If your current paycheck shows $2,000 but the YTD column shows $24,000, you have earned $24,000 since the start of the year across all pay periods combined. YTD resets to zero every January 1, not on your hire date.

Almost every line on your pay stub appears twice: a current-period amount and a YTD amount beside it. Most people glance at the current number and ignore the rest. But the YTD column is where you catch payroll errors, verify your tax withholding, track when Social Security stops, and prove your income to a lender. This guide breaks down every YTD field and shows how to read and verify yours.

What YTD Means and Why It Is Bigger Than Your Paycheck

The most common reaction to the YTD column is confusion: why is this number so much larger than what I just got paid? The answer is simple. Your current-period column shows what you earned in this one pay period. The YTD column shows everything you have earned since January 1, added up across every paycheck so far this year.

If you are paid biweekly and you are looking at your twelfth paycheck of the year, your YTD gross is roughly twelve times a single check. By December, it represents your entire annual earnings. Every line on your stub that carries a current-period figure -- gross pay, each tax, each deduction, net pay -- also carries a YTD running total beside it.

The two columns answer different questions. The current column tells you what happened this period. The YTD column tells you where you stand for the year. For a detailed walkthrough of how to read the two columns side by side and what to check in each, see current versus YTD columns on a pay stub.

The Four YTD Fields on Your Pay Stub

Your pay stub tracks a separate YTD running total for every category. Four of them matter most:

| YTD Field | What It Tracks |

|---|---|

| YTD Gross | Everything you earned before deductions since January 1 -- base salary or wages, overtime, bonuses, and commissions. This is the figure lenders and landlords ask for. |

| YTD Taxes | Combined federal income tax, state and local tax, and FICA (Social Security and Medicare) withheld so far this year. |

| YTD Deductions | Cumulative non-tax amounts -- health insurance premiums, 401(k) contributions, HSA, and any other benefit deductions since January 1. |

| YTD Net | Your total take-home pay for the year so far -- YTD gross minus YTD taxes and YTD deductions. This is what actually reached your bank account. |

Each tax and each deduction also has its own individual YTD line, so you can see exactly how much has gone to federal tax, to Social Security, to your 401(k), and so on. For a full breakdown of what every deduction label means, see pay stub deduction codes.

When Does YTD Reset? Calendar Year vs Fiscal Year

For almost everyone, YTD resets to zero on January 1 and runs through December 31. The calendar year is the standard for personal pay stubs because it aligns with the tax year the IRS uses for your W-2.

A small number of employers run an internal fiscal year that begins on a different date -- July 1 is a common choice for some organizations. If your employer uses a fiscal year, internal reports may calculate YTD from that alternate start date. Your tax-related YTD figures still follow the calendar year for W-2 purposes. If you are unsure which your stub uses, ask your HR or payroll department.

Why YTD Matters: It Tracks When Social Security Withholding Stops

The most practical reason to watch your YTD gross is that it tells you when your Social Security tax will stop. Social Security (the 6.2% OASDI line) only applies to the first $184,500 of wages in 2026. Once your YTD gross crosses that threshold, the Social Security line stops climbing for the rest of the year, and your take-home pay jumps noticeably.

YTD tracking matters for two other thresholds as well. Your YTD 401(k) line shows how close you are to the 2026 contribution limit of $24,500. And your YTD gross determines when the Additional Medicare Tax of 0.9% begins, once wages cross $200,000. For the full mechanics of FICA, the wage base, and what happens when withholding stops mid-year, see what FICA means on a pay stub.

How to Calculate and Verify Your YTD

You do not need payroll software to check your YTD. The math is simple: multiply your gross pay per period by the number of pay periods that have passed this year. The result should match the YTD gross on your most recent stub.

YTD Verification Example -- Biweekly Employee, Late June

If your actual YTD gross matches that figure, your pay is tracking correctly. If there is a meaningful gap, something is off -- a missing bonus, uncredited overtime, or a pay period processed incorrectly. A quick mid-year sanity check: by late June, your YTD gross should be roughly half your annual salary, adjusted for any bonuses or overtime. If it is well short of that, contact payroll.

Using YTD as Proof of Income

When you apply for a loan or an apartment, the YTD figure on your pay stub is one of the first things the reviewer scans. It confirms that your income is consistent across the year rather than a single high paycheck.

A few things lenders and landlords look for:

| What They Check | Why It Matters |

|---|---|

| YTD gross income | Confirms steady annual earnings, not a one-time spike. They qualify you on gross, not take-home. |

| 3x rent rule (landlords) | Most landlords require gross monthly income of at least three times the monthly rent. |

| Number of stubs | Most lenders want two to three recent stubs; mortgage lenders typically want about 30 days of stubs. |

| Recency | Stubs should be dated within 30 days of your application, showing employer name and pay period. |

If you are an employee, your payroll portal already produces stubs with YTD totals. If you need a clean, properly formatted record for an application, you can generate a pay stub with accurate YTD totals that documents your real earnings.

YTD for Freelancers and the Self-Employed

If you are a freelancer or 1099 contractor, no employer tracks YTD for you. That responsibility is yours. Your YTD is simply the total of everything you have invoiced and been paid since January 1, tracked in your own records.

YTD tracking matters most for one reason: quarterly estimated taxes. The IRS expects self-employed workers to pay taxes throughout the year, not in a single lump sum, using Form 1040-ES. Your YTD net income is the figure you use to size each payment.

| 2026 Quarterly Deadline | Covers Income From |

|---|---|

| April 15, 2026 | January 1 -- March 31 |

| June 16, 2026 | April 1 -- May 31 |

| September 15, 2026 | June 1 -- August 31 |

| January 15, 2027 | September 1 -- December 31 |

Under the IRS safe harbor rule, you generally need to pay the lesser of 90% of your current-year tax or 100% of what you owed last year -- rising to 110% if your prior-year adjusted gross income exceeded $150,000. A quick withholding check for anyone: divide your YTD federal tax by your YTD gross to get your effective withholding rate, then compare it to your expected tax bracket. If the rate is well below your bracket, you may be under-withholding and could owe at filing. The IRS Self-Employed Tax Center has the full estimated-tax worksheets.

How YTD Connects to Your W-2

Your final pay stub of the year is the bridge to your W-2. The YTD gross on that last December stub should reconcile to W-2 Box 1, and your YTD federal tax withheld should match Box 2.

One detail trips people up: YTD gross is often higher than W-2 Box 1. That is expected. Pre-tax deductions -- traditional 401(k), health insurance, HSA -- reduce your taxable wages but not your gross earnings. So your YTD gross shows everything you earned, while Box 1 shows only what was taxable. Both numbers are correct; they measure different things. For the full box-by-box reconciliation and how each deduction affects each W-2 box, see pay stub deduction codes and your taxable wages.

Common YTD Errors to Watch For

Even with modern payroll software, YTD errors happen. The most frequent ones:

| Error | What to Check |

|---|---|

| Thinking YTD equals your current paycheck | The top confusion. YTD is cumulative since January 1, not this period only. |

| Missing bonus, overtime, or commission | If a bonus is not reflected in YTD gross, the figure understates your true earnings. Confirm every form of pay appears. |

| Missing benefit deduction | If a new 401(k) or health plan does not show in YTD deductions from your enrollment date, contact payroll. |

| January carryover | Your first stub of the year should show only that period. Carryover from the prior year means payroll was not closed out -- flag it immediately. |

If anything looks off, compare your current stub to the previous one to isolate the line that changed, then contact payroll in writing with the specific figure and pay date.

Frequently Asked Questions About YTD

YTD stands for year-to-date. It is the cumulative total of a line item -- earnings, taxes, or deductions -- from January 1 through your most recent pay period. It resets to zero each January 1.

Your paycheck shows one pay period. YTD shows everything you have earned or had withheld since January 1. If you are paid biweekly and are on your twelfth check, your YTD is roughly twelve times a single check.

January 1 for almost everyone. Even if you started mid-year, YTD resets the following January 1. A small number of employers track an internal fiscal year that starts on a different date, so check with HR if you are unsure.

Your final December stub's YTD gross should match W-2 Box 1 after pre-tax deductions, and your YTD federal tax should match Box 2. YTD gross is often higher than Box 1 because pre-tax deductions like 401(k) and health insurance reduce taxable wages. Both figures are correct -- they measure different things.

Multiply your gross pay per period by the number of pay periods elapsed this year. The result should match your YTD gross. If there is a meaningful gap, contact payroll -- a missing bonus, overtime, or a processing error is the usual cause.

Yes. Lenders and landlords use YTD gross to confirm consistent annual income rather than a one-time spike. Most want two to three recent stubs dated within 30 days of your application. They qualify you on gross income, not take-home pay.

$11,439, which is 6.2% of the $184,500 Social Security wage base for 2026. If your YTD Social Security line exceeds that amount, your employer has over-withheld and is required to refund the excess.