How to Read a Pay Stub: Labeled Example of Earnings, Taxes and Deductions

By ePaystubs Editorial Team | Updated June 22, 2026 | Verified against IRS Topic 751

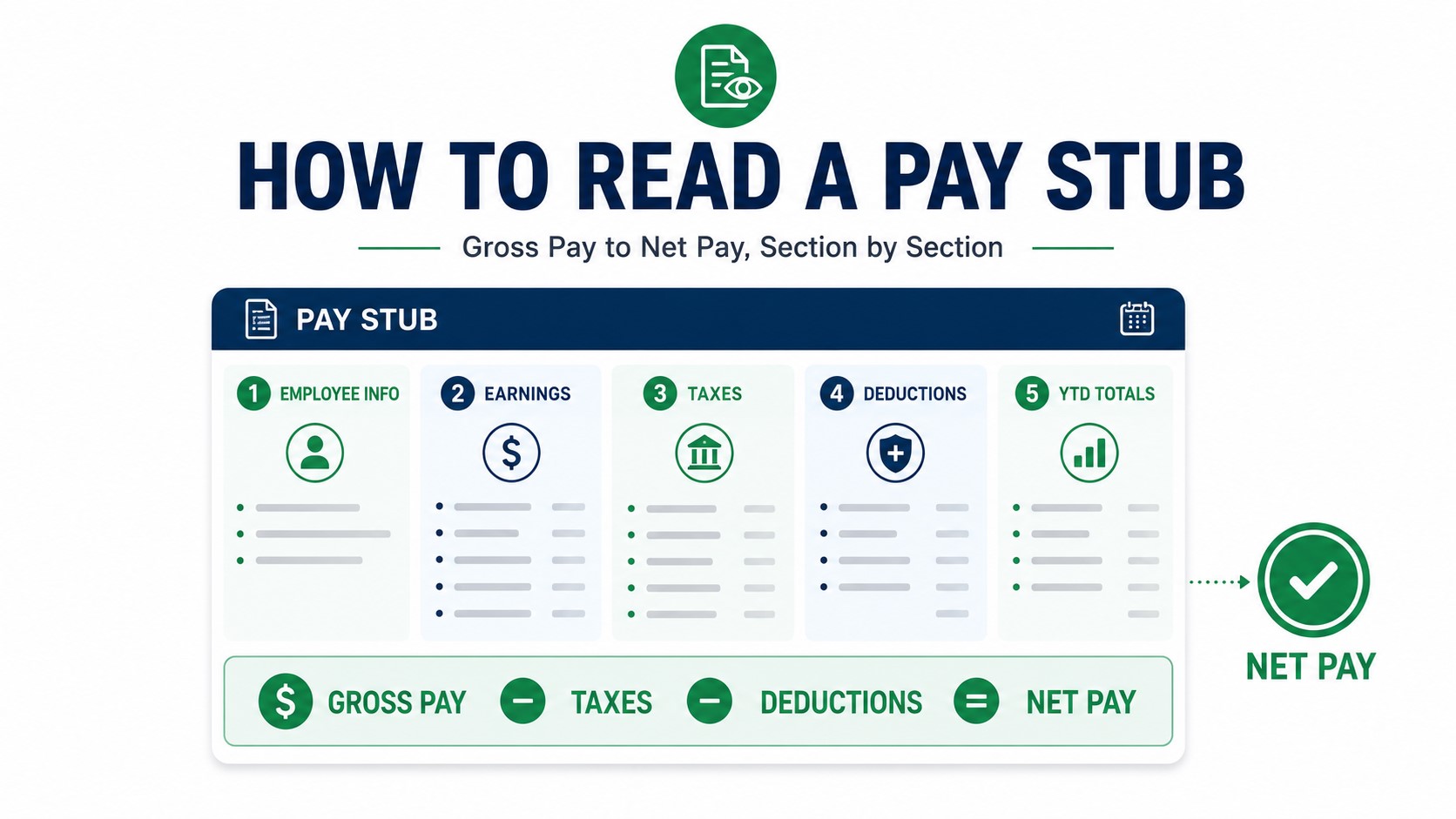

A pay stub shows how your gross pay becomes your take-home pay through taxes and deductions. To read one, scan three numbers first: your gross pay (were you paid for the right hours?), your total taxes and deductions (do they look right?), and your net pay (does it match your deposit?). Everything else on the stub explains how you got from the first number to the last. Below, a labeled sample stub breaks down every section in plain English.

Almost everyone has felt the small shock of a first paycheck landing lower than expected. The pay stub is the document that explains the gap. It is a complete record of what you earned, what was taken out, and why. This guide walks through a labeled sample stub section by section, clears up the difference between a pay stub, a paycheck, and a W-2, and shows you how to check your own stub for errors.

- Labeled sample stub

- Pay stub vs paycheck vs W-2

- Header info

- Earnings

- Tax withholdings

- Deductions

- Year-to-date

- Gross to net example

- Check for errors

- Required by law?

The Labeled Pay Stub: Every Section at a Glance

Here is a typical US pay stub with each section numbered. The exact layout varies by employer and payroll system, but the underlying information is always the same. Match each number on the stub to the key below it.

Labeled Pay Stub Reference

1 Sample Co. Inc.

| Earnings | Rate | Hours | Current | YTD |

|---|---|---|---|---|

| Regular (REG) | $34.62 | 80.00 | $2,769.23 | $33,230.76 |

| Overtime (OT) | $51.93 | 2.00 | $103.85 | $622.80 |

| Gross Pay | $2,873.08 | $33,853.56 |

| Tax | Current | YTD | ||

|---|---|---|---|---|

| Federal Income Tax (FIT) | $331.00 | $3,900.00 | ||

| Social Security (OASDI) | $178.13 | $2,098.92 | ||

| Medicare (MED) | $41.66 | $490.88 | ||

| OH State Income Tax (SIT) | $78.50 | $924.00 |

| Deduction | Current | YTD | ||

|---|---|---|---|---|

| Health Insurance (pre-tax) | $115.38 | $1,384.56 | ||

| 401(k) (pre-tax) | $143.65 | $1,692.68 | ||

| Roth 401(k) (post-tax) | $57.46 | $677.04 |

| 9Net Pay (this period) | $1,926.30 | 10YTD → |

1

2

3

4

5

6

7

8

9

10

Every section below explains one of these zones in more detail and links to a focused guide if you want to go deeper.

Pay Stub vs Paycheck vs W-2: Clearing Up the Confusion

Three documents get mixed up constantly. Knowing the difference makes the rest of this guide click.

| Document | What It Is | When You Get It |

|---|---|---|

| Paycheck | The actual payment, by direct deposit or physical check. It is the net (take-home) amount. | Each pay period |

| Pay stub | The document accompanying the paycheck that itemizes how your gross pay became net pay. | Each pay period, with the paycheck |

| W-2 | The annual tax form summarizing your full-year taxable wages and taxes withheld, used to file your return. | Once a year, by late January |

Two of these distinctions trip people up most often. For a closer look at how a pay stub differs from the paycheck itself, and which one actually works as proof of income, see pay stub vs paycheck. And for how a pay stub differs from your W-2, why each is used at tax time, and why their numbers do not line up, see pay stub vs W-2.

One key point connects the pay stub and the W-2: your final stub of the year carries YTD totals that reconcile to your W-2, but the gross figures will usually not match, because pre-tax deductions lower the taxable wages reported on the W-2. That gap is normal. For exactly why and how the numbers reconcile, see taxable wages on a pay stub.

Section 1: Header and Identifier Information

The top block of the stub identifies the people and the period involved: your employer's name and address, your own name and address, your employee ID, a masked Social Security number, the pay period dates, and the pay date. None of this affects your pay math, but it matters. If your name, address, or Social Security number is wrong, it can cause problems with your direct deposit or your tax filing, so report any error here to HR right away.

Section 2: Earnings (Your Gross Pay)

This is the "money in" section, and everything in it adds up to your gross pay. For salaried employees, gross pay is your annual salary divided by the number of pay periods (26 for biweekly, 24 for semi-monthly, 12 for monthly). For hourly employees, it is your hours worked times your rate, plus any overtime, which is paid at 1.5 times your regular rate for hours over 40 in a week.

You will often see several earnings codes here: REG (regular), OT (overtime), HOL (holiday), PTO (paid time off), BONUS, and COMM (commission), among others. Each is a different form of pay that counts toward your gross. For a complete glossary of every earnings code and abbreviation you might encounter, see pay stub abbreviations.

Section 3: Tax Withholdings

This is where the mandatory taxes come out. There are three or four lines, depending on where you live:

Federal income tax is withheld based on your W-4 elections (filing status, dependents, extra withholding) using IRS tables, and ranges across seven brackets from 10% to 37%. State income tax appears where applicable, though nine states have none. FICA is the combination of Social Security and Medicare.

Together, the typical breakdown is roughly 7.65% to FICA, 10% to 22% to federal income tax, and 0% to 13% to state tax, which is a large part of why take-home pay lands well below gross. A few cities (New York City, Philadelphia, and several Ohio cities) also levy a local income tax that appears as its own line. For the full mechanics of FICA, why it shows as two separate lines, and what happens when Social Security withholding stops mid-year, see what FICA means on a pay stub.

Section 4: Deductions (Pre-Tax and Post-Tax)

After taxes come deductions, which fall into two groups that are taxed very differently. Pre-tax deductions (health insurance, a traditional 401(k), HSA, and FSA) come out before taxes are calculated, lowering your taxable income. Post-tax deductions (a Roth 401(k), union dues, and garnishments) come out after taxes are already withheld.

A quick rule for the codes: A code ending in EE is your portion, taken from your pay. A code ending in ER is your employer's contribution, shown for transparency, and it does not reduce your take-home pay. You may also see GTL (group-term life), which is not a deduction at all but imputed income added to your wages when employer life insurance exceeds $50,000.

The difference between pre-tax and post-tax matters more than most people realize, since it changes both your take-home pay now and your tax treatment later. For which deductions are pre-tax versus post-tax and when paying tax now is the smarter choice, see pre-tax versus post-tax deductions. For what every individual deduction code means and exactly how each one is taxed, see pay stub deduction codes.

Section 5: Year-to-Date (YTD) Totals

Almost every line on your stub shows two numbers: the current amount and the YTD amount beside it. YTD stands for year-to-date, the running total of that figure from January 1 through your most recent paycheck. It is why the YTD column looks so much bigger than your single paycheck, and it resets to zero every January 1, not on your hire date.

The YTD column has three practical uses: it serves as proof of income for lenders and landlords, it lets you watch your wages approach the Social Security wage base, and it is how you verify your final stub against your W-2. For how YTD works in detail, how to verify it, and how to use it as proof of income, see what YTD means on a pay stub.

A Worked Example: From Gross to Net

Here is how the whole stub comes together for a single filer earning $75,000 a year, paid biweekly. Each paycheck starts at a gross of $2,884.62, and the deductions bring it down to take-home pay.

| Line | Amount (per paycheck) |

|---|---|

| Gross pay | $2,884.62 |

| Federal income tax | -$345.00 |

| Social Security (6.2%) | -$178.85 |

| Medicare (1.45%) | -$41.83 |

| State income tax | -$135.00 |

| 401(k), pre-tax | -$173.08 |

| Health insurance, pre-tax | -$115.00 |

| Net pay (take-home) | $1,895.86 |

That take-home figure is about 66% of gross pay, with the other third going to taxes and benefits before the money ever reaches the bank. The exact split depends on your state, your W-4, and your benefit choices. These figures are a simplified illustration of how the pieces fit together, not exact withholding for any individual. For the detailed math behind how pre-tax deductions shape your taxable wages, see taxable wages on a pay stub.

How to Check Your Pay Stub for Errors

Reading your stub is most useful when you use it to catch mistakes. Run through these checks each pay period, and especially after any change to your pay or benefits:

- Multiply your hours by your rate (adding overtime at 1.5 times for hours over 40) and confirm it matches your gross pay.

- Compare your deductions to your last stub. Did any amount change without an explanation?

- Confirm your net pay matches your bank deposit exactly.

- Check that your YTD totals are climbing at the rate you expect.

- If anything does not reconcile, contact payroll or HR in writing, noting the specific amount and pay date.

If you see a code you do not recognize, do not guess, especially in the deductions section. Check your stub's legend or your benefits paperwork, or ask HR, and use our pay stub abbreviations guide as a reference. Most states require employers to correct genuine wage errors promptly once they are notified.

Are Pay Stubs Required by Law?

Most states require employers to provide some form of pay stub or itemized wage statement, whether on paper or electronically. A few states, including Alabama, Arkansas, Florida, and Mississippi, have no specific pay stub law. Even in those states, the federal Fair Labor Standards Act requires employers to keep accurate records of hours worked and wages paid.

It is worth keeping your own copies as well. The general guidance is to keep at least three years of pay stubs on file, and longer if your state requires it, since you may need them to verify your W-2, apply for a loan, or resolve a discrepancy. Because the specific rules and taxes vary from state to state, see your state's pay stub guide for the details that apply where you work.

Where to Find Your Pay Stub

Most employers deliver pay stubs digitally through a payroll portal or mobile app, such as ADP, Gusto, Paychex, or Workday. Look for a self-service site where you can view and download each period's stub as a PDF. If you receive paper stubs, the fields and layout are the same. If you cannot find yours, contact your HR or payroll department.

If you are self-employed, a freelancer, or you need a clean, properly formatted pay stub for proof of income, you can generate a pay stub with all the standard fields covered in this guide.

Frequently Asked Questions

Start with three numbers: gross pay (your total earnings), total taxes and deductions (what was withheld), and net pay (your take-home). Then work through the five sections, header, earnings, taxes, deductions, and year-to-date totals, to see exactly how your gross pay became your net pay.

A paycheck is the actual payment, whether direct deposit or a physical check, and it is the net amount. A pay stub is the document that comes with it, itemizing your earnings, taxes, and deductions. You receive both each pay period.

Taxes and deductions typically take 25% to 40% of gross pay before you see it. That includes federal income tax, Social Security and Medicare (7.65%), state tax where applicable, and any pre-tax benefits like health insurance and retirement contributions.

YTD stands for year-to-date, the running total of a figure from January 1 through your current paycheck. It resets to zero each January 1. For a full explanation, see our guide on what YTD means on a pay stub.

Not exactly. Your pay stub shows gross earnings; your W-2 shows taxable wages after pre-tax deductions. Your final stub's YTD totals reconcile to your W-2, but the gross figures will usually differ. This is normal and correct.

Compare the stub to your previous one to find what changed, then contact payroll or HR in writing with the specific amount and pay date. Most states require employers to correct genuine wage errors promptly once notified.

Most states require it, though a few (Alabama, Arkansas, Florida, Mississippi) have no specific pay stub law. Even where stubs are not mandated, the federal Fair Labor Standards Act requires employers to keep accurate pay records.

Explore the Full Pay Stub Guide

Go deeper on any section of your pay stub with these focused guides.