What Is Proof of Income? Documents, Examples and How to Show It

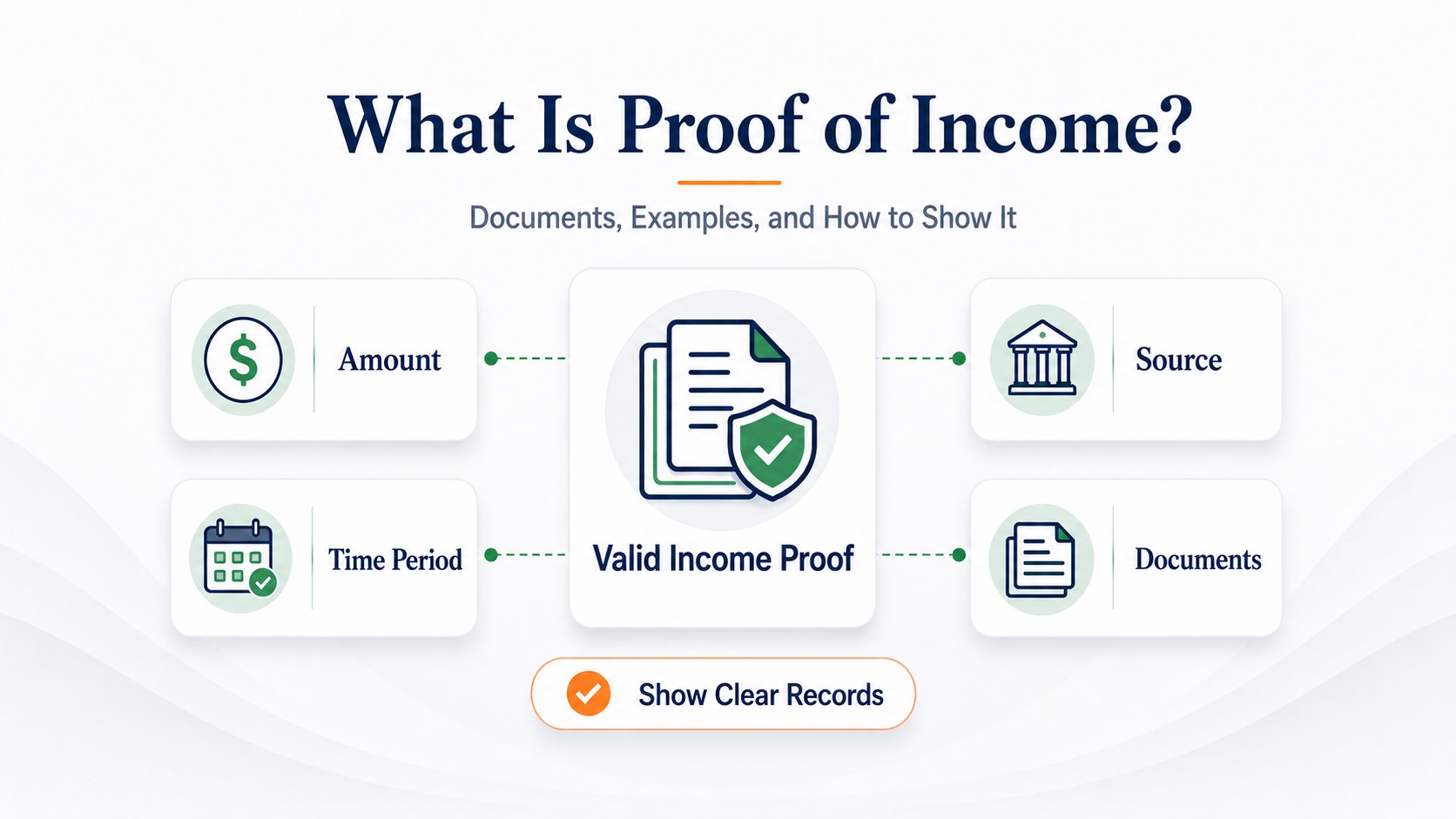

Proof of income is official documentation that shows how much money you earn. Whatever document you use, a valid one confirms three things: the amount you earn, the source of that income, and the time period it covers. The most accepted documents are pay stubs, tax returns, W-2s, 1099s, bank statements, and benefit or verification letters, and most landlords and lenders ask for two or three together. Which documents work best depends on how you earn, this guide maps every situation.

Proof of income comes up at nearly every major financial step: renting a place, taking out a loan, applying for benefits, even some immigration and court processes. The request can feel vague, but the underlying standard is consistent, and once you understand it, choosing the right document is simple. This guide is the complete overview: what proof of income is, what counts, what doesn't, and exactly which documents to use for your situation, with detailed guides linked for each path. We're a pay-stub resource, so we'll be clear and practical throughout.

- What it is

- What it isn't

- Why you need it

- The documents

- By situation

- How much you need

- Keeping it legitimate

What Proof of Income Is (and the Three Things It Must Show)

Proof of income is any official document that confirms how much money you earn. The reason so many different documents qualify is that they all do the same job: a valid proof of income answers three questions.

Any document that satisfies all three, the amount, the source, and the time period, will generally be accepted. Most reviewers also want it to be recent, typically covering the last 30 to 90 days. Lenders, landlords, and government agencies all ask for proof of income for the same reason: to confirm you can meet a financial obligation before they approve a loan, a lease, or a benefit.

What Proof of Income Is NOT

Two clarifications save a lot of confusion, and knowing them signals that you understand what reviewers actually want.

Proof of income vs proof of funds

Proof of income shows your ongoing earnings, money that regularly comes in. Proof of funds shows the savings or assets you have available right now. They answer different questions, and most applications want income (to confirm recurring payments), though some ask for both.

What does not count

Photos of cash, handwritten notes, unofficial spreadsheets, and promises of future earnings are not accepted. Documents older than about three months usually won't work either, and payment-app screenshots (PayPal, Venmo) generally aren't enough on their own. Use original, unaltered documents.

Why You Need Proof of Income

You'll be asked for proof of income any time another party needs to judge your financial stability. The most common situations:

| Situation | Why proof of income is needed |

|---|---|

| Renting | Landlords confirm you can cover the rent |

| Borrowing | Lenders assess repayment for loans, mortgages, car loans, and credit cards |

| Benefits | Agencies check eligibility for assistance and subsidies |

| Immigration | Financial-solvency evidence for visas and residence |

| Employment | Salary verification during onboarding |

| Court matters | Calculating child support or alimony |

The Documents That Count (Ranked by How Much They're Trusted)

Many documents work, but they don't all carry equal weight. Here is the toolkit, organized by how much trust each one earns.

| Tier | Documents | Why |

|---|---|---|

| Strongest | Tax return (1040), W-2, 1099 | Government-recorded, hard to falsify, cover a full year |

| Strong | Pay stubs, verification or offer letters, bank statements | Employer-issued or bank-issued; show current income |

| Supporting | P&L, invoices, benefit letters, court orders, payment apps | Strong in context; often paired, some not standalone |

Most landlords and lenders ask for two or three documents that corroborate each other, the goal is consistent figures across documents, not one perfect record. When a document shows year-to-date earnings, that running total is often what a reviewer checks first, so it helps to understand what your YTD figure means.

Proof of Income by Situation

The right documents depend on how you earn and what you're applying for. Find your situation below, and follow the link for the full detail.

How Much Income You Need

Beyond proving income, you usually have to show you earn enough. Reviewers use two tests, and which one applies depends on whether you're renting or borrowing.

Keeping It Legitimate

Whatever documents you use, they have to be accurate and unaltered. Recipients cross-check them, against the IRS, your employer, and your bank data, and your names and figures need to match across every document you submit.

The Bottom Line

Proof of income shows three things: the amount you earn, its source, and the time period it covers. The strongest proof is two or three trusted documents that corroborate each other, IRS forms carry the most weight, followed by employer documents and bank statements. Which you use comes down to your situation, and the linked guides cover each one in full.

If you have real income but no formatted pay stub, you can create one from your true earnings as one document in your set, matched to your other records. The goal is always documentation that reflects what you actually earn.

Frequently Asked Questions

Proof of income is official documentation that shows how much you earn. A valid document confirms three things: the amount you earn, the source of that income, and the time period it covers. Common examples include pay stubs, tax returns, W-2s, 1099s, bank statements, and verification letters.

Pay stubs, tax returns (1040), W-2s, 1099s, bank statements, employer verification letters, offer letters, and benefit award letters all count. The strongest are IRS-issued forms, followed by employer documents and bank statements. Most landlords and lenders ask for two or three together.

Proof of income shows your ongoing earnings, how much money regularly comes in. Proof of funds shows the savings or assets you currently have available. Lenders and landlords usually want proof of income to confirm you can make recurring payments, though some situations call for both.

Photos of cash, handwritten notes, unofficial spreadsheets, promises of future earnings, and documents older than about three months are generally not accepted. Payment-app screenshots like PayPal or Venmo usually aren't enough on their own without official tax documents or bank statements to back them up.

Lead with your tax returns and bank statements, plus 1099s and a profit-and-loss statement. Lenders and landlords want to see consistent income over time. See our guide on proof of income when self-employed for the full approach.

Combine documents that fit how you earn, tax returns, bank statements, 1099s, benefit letters, or an employer verification letter. See our guide on how to show proof of income without pay stubs for every situation, including benefits, cash income, and a new job.

Most landlords and lenders ask for two or three documents that corroborate each other, for example, a tax return plus recent bank statements. The goal is consistent figures across documents that confirm both your income level and that it's recent.